What Is an IRS 1099 Form?

If you have ever worked as a freelancer, earned interest from a savings account, collected rent on a property, or sold investments through a brokerage, you have probably asked yourself: "What Is an IRS 1099 Form?" You are not alone. Millions of taxpayers receive these forms each January, and many find them confusing at first glance. The good news is that IRS 1099 forms follow a logical structure once you understand the basics. This guide explains everything you need to know about Form 1099, from who receives one to how different types work, what backup withholding means, and how freelancers and independent contractors should use these forms for accurate tax reporting.

All information in this article aligns with official IRS guidance. The IRS issues Form 1099 as part of its information reporting system, which helps the agency verify that taxpayers report all taxable income. For complete details, always refer to https://www.irs.gov/forms-pubs/about-form-1099-misc and the official instructions for each specific 1099 variant.

An IRS 1099 form is a tax document businesses use to report certain types of income paid to nonemployees, freelancers, contractors, investors, and vendors. Form 1099 helps the IRS track taxable income that is not reported on a traditional employee W-2 form. Each 1099 variant covers a specific income category.

Table of Contents

What Is an IRS 1099 Form?

An IRS 1099 form is part of a family of tax documents officially called "information returns." According to the IRS, Form 1099 documents payments made during the tax year by an individual or a business that is not your employer. Unlike a W-2, which reports wages where taxes are already withheld by an employer, a 1099 typically reports income where no tax has been taken out yet. The responsibility for reporting that income and paying any taxes owed rests with the recipient.

The IRS 1099 series covers many types of income. Some forms report nonemployee compensation paid to independent contractors. Others report interest from bank accounts, dividends from investments, proceeds from stock sales, distributions from retirement accounts, unemployment compensation, and even canceled debt. Each 1099 variant has its own form number and specific reporting rules.

IRS guidance explains that the purpose of these forms is twofold. First, they provide taxpayers with a record of income they must include on their tax returns. Second, they provide the IRS with the same information so the agency can match what taxpayers report against what payers say they paid. This matching program helps the IRS detect underreported income and refund fraud.

Key Point: Receiving a 1099 does not automatically mean you owe tax on that amount. It simply tells you what income was reported to the IRS under your name or Taxpayer Identification Number. You may have deductions, expenses, or credits that reduce or eliminate the tax owed on that income.

Who Receives a 1099 Form?

Many different people receive 1099 forms each year. If you fall into any of the following categories, there is a good chance you will find at least one 1099 in your mailbox or inbox before January 31. Common recipients include:

Freelancers and Independent Contractors

If you performed services for a business and earned $600 or more during the tax year (or $2,000 starting in tax year 2026), you should receive Form 1099-NEC. This includes gig workers, rideshare drivers, freelance writers, graphic designers, consultants, and anyone paid as a nonemployee.

Landlords and Property Owners

If you collected rent from tenants who operate a trade or business, and the payments met the reporting threshold, you may receive Form 1099-MISC reporting those rental payments.

Investors and Savers

Anyone who earned interest from a bank account (Form 1099-INT), dividends from stocks (Form 1099-DIV), or sold securities through a brokerage (Form 1099-B) will receive the appropriate 1099.

Retirees and Benefit Recipients

Distributions from retirement accounts trigger Form 1099-R. Social Security recipients receive Form SSA-1099. Unemployment compensation recipients receive Form 1099-G.

According to the IRS, most 1099 forms must be furnished to recipients by January 31 of the year following the tax year being reported. This early deadline gives taxpayers time to gather all their income documents before the April tax filing deadline.

Types of 1099 Forms Explained

The IRS maintains a series of 1099 forms, each designed for a specific type of income. Understanding which form applies to your situation is essential for accurate tax reporting. Here are the most common 1099 form types:

| Form Number | What It Reports | Common Example | Recipient Due Date |

|---|---|---|---|

| 1099-NEC | Nonemployee compensation | Freelance work, contractor payments | January 31 |

| 1099-MISC | Rents, royalties, prizes, medical payments, attorney fees, and other miscellaneous income | Rent paid for office space | February 1 (or February 16 for certain payments) |

| 1099-INT | Interest income | Savings account interest | January 31 |

| 1099-DIV | Dividends and distributions | Stock dividends | January 31 |

| 1099-B | Proceeds from broker and barter exchange transactions | Stock sales | February 15 |

| 1099-G | Government payments | Unemployment benefits, state tax refunds | January 31 |

| 1099-R | Retirement plan distributions | Pension or IRA withdrawals | January 31 |

| 1099-K | Payment card and third-party network transactions | Credit card sales, PayPal business payments | January 31 |

| 1099-S | Proceeds from real estate transactions | Home sale | February 15 |

| 1099-C | Cancelation of debt | Foreclosure, short sale, or debt settlement | January 31 |

The two forms that generate the most questions are Form 1099-MISC and Form 1099-NEC. Let us examine each one in detail.

1099-MISC vs 1099-NEC: Understanding the Difference

Before tax year 2020, businesses used Form 1099-MISC to report almost all non-wage payments, including payments to independent contractors. Starting in 2020, the IRS reintroduced Form 1099-NEC specifically for reporting nonemployee compensation. This change separated contractor payments from other types of miscellaneous income and gave each form its own filing deadline.

Form 1099-NEC: Nonemployee Compensation

Form 1099-NEC reports payments made to individuals who are not your employees. This includes fees, commissions, prizes, and awards for services performed by independent contractors, freelancers, and gig workers. If you hire someone to design a website, repair equipment, or provide consulting services, and they are not on your payroll, you report those payments on Form 1099-NEC.

The key deadline for Form 1099-NEC is January 31 for both recipient copies and IRS filing, regardless of whether you file electronically or on paper. This is a hard deadline with no automatic extension available.

Form 1099-MISC: Miscellaneous Information

Form 1099-MISC now reports a variety of payments that are not compensation for services. According to the IRS, you must file Form 1099-MISC for each person to whom you have paid during the year at least $10 in royalties or broker payments, or at least $600 in rents, prizes and awards, other income payments, medical and health care payments, crop insurance proceeds, cash payments for fish, payments to an attorney, and fishing boat proceeds. You also use it to report direct sales of at least $5,000 of consumer products for resale.

The IRS deadline for furnishing Form 1099-MISC to recipients is February 1 (or February 16 for certain payments). Paper filing with the IRS is due February 28, and electronic filing is due March 31.

The December 2026 revision of Form 1099-MISC, available at https://www.irs.gov/pub/irs-pdf/f1099msc.pdf, includes updated boxes for cash tips (Box 13a), Treasury Tipped Occupation Code (Box 13b), overtime compensation (Box 14), and nonqualified deferred compensation (Box 15). These changes reflect provisions enacted under recent tax legislation.

When Is a 1099 Required?

Businesses are required to issue a 1099 form when they make certain types of payments that meet or exceed IRS reporting thresholds. The specific threshold depends on the type of payment and the form being used.

2025 Tax Year Thresholds (Forms Filed in Early 2026)

- Form 1099-NEC: $600 or more in nonemployee compensation

- Form 1099-MISC: $600 or more for most payment types; $10 or more for royalties

- Form 1099-INT: $10 or more in interest

- Form 1099-K: More than $20,000 and more than 200 transactions (for third-party network transactions)

2026 Tax Year Thresholds (Forms Filed in Early 2027)

Beginning with the 2026 tax year, the reporting thresholds for Forms 1099-NEC and 1099-MISC increase from $600 to $2,000. This change was enacted under the One Big Beautiful Bill Act signed into law on July 4, 2025. The $2,000 threshold will be adjusted for inflation beginning in 2027. The 1099-K threshold remains at more than $20,000 and more than 200 transactions.

Importantly, the IRS reminds taxpayers that reporting thresholds do not affect whether income is taxable. Even if a payer does not send you a 1099 because your payments fell below the threshold, you are still legally required to report all taxable income on your tax return.

How Businesses Use Form 1099

For businesses, issuing 1099 forms is not optional. It is a legal compliance requirement. According to the IRS, any business that makes reportable payments during the tax year must file the appropriate 1099 form for each payee. The business must send Copy B to the recipient and file Copy A with the IRS.

Here is a step-by-step overview of the 1099 issuance process from a business perspective:

Collect W-9 Forms

Before paying a vendor or contractor, request a completed Form W-9 to obtain their legal name, Taxpayer Identification Number, and business classification.

Track Payments Throughout the Year

Maintain accurate records of all payments made to each vendor or contractor, including dates and amounts.

Determine Reporting Obligation

At year-end, identify which payees received reportable payments meeting or exceeding the applicable threshold.

File Forms with the IRS and Furnish to Recipients

Complete the appropriate 1099 form, file it with the IRS by the deadline, and provide a copy to each recipient.

Businesses that fail to file required 1099 forms or file them late face penalties. The IRS penalty structure for 2026 starts at $60 per form if filed within 30 days of the due date, increases to $130 per form if filed more than 30 days late but by August 1, and rises to $330 per form if filed after August 1 or not filed at all. Intentional disregard can result in penalties of at least $680 per form. For small businesses, annual penalty caps apply.

See How Self-Employment Taxes Affect Your Income

If you receive a 1099-NEC as a freelancer or independent contractor, you are responsible for self-employment taxes in addition to income tax. Use the paycheck calculator to estimate your take-home pay after taxes and plan for your quarterly estimated tax payments.

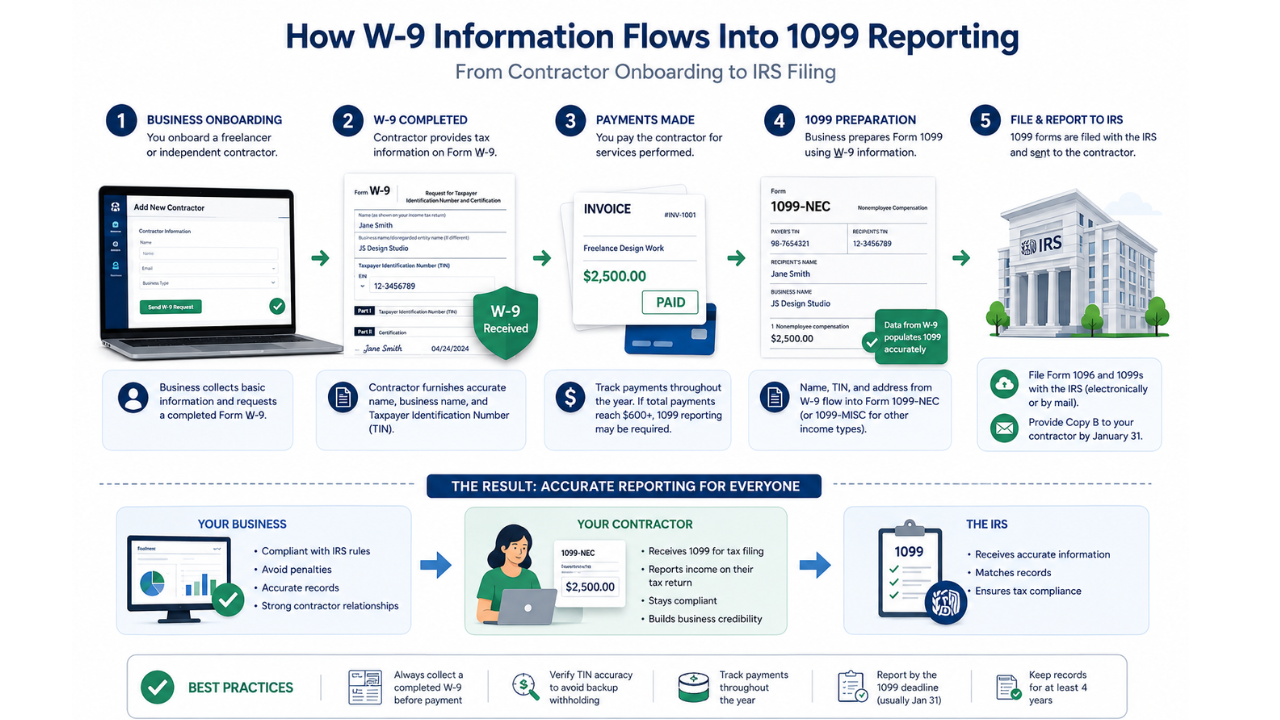

Calculate Your Take-Home Pay NowHow W-9 and 1099 Forms Work Together

Form W-9 and Form 1099 are two sides of the same tax reporting coin. A W-9 is the form a business collects from a vendor or contractor before making payments. The 1099 is the form the business issues after the end of the tax year summarizing those payments. The information collected on the W-9 flows directly into the 1099.

Specifically, Form W-9, officially titled "Request for Taxpayer Identification Number and Certification," collects the following information that populates a 1099:

- Legal Name: The payee's name as it appears on their tax return.

- Taxpayer Identification Number (TIN): Either a Social Security Number (SSN) for individuals, an Employer Identification Number (EIN) for businesses, or an Individual Taxpayer Identification Number (ITIN) for certain non-citizens.

- Business Classification: Whether the payee is a sole proprietor, corporation, partnership, LLC, or other entity type.

- Address: The payee's mailing address.

IRS guidance explains that the W-9 serves as the payer's primary source of certified taxpayer information. Without a properly completed W-9, a business cannot accurately prepare a 1099. This is why most businesses request a W-9 during the vendor onboarding process, well before any payments are made.

Taxpayer Identification Number (TIN) Explained

A Taxpayer Identification Number, or TIN, is the unique number the IRS uses to identify taxpayers. Every 1099 form must include the recipient's correct TIN. The IRS cross-references the TIN and name combination on each 1099 against its database to ensure income is properly attributed.

Social Security Number (SSN)

Used by individual taxpayers, including sole proprietors who have not obtained an EIN. This is a nine-digit number issued by the Social Security Administration.

Employer Identification Number (EIN)

Used by businesses, partnerships, corporations, LLCs, and estates. Also called a Federal Tax Identification Number. Sole proprietors may obtain an EIN to avoid sharing their SSN with clients.

Individual Taxpayer Identification Number (ITIN)

Used by individuals who are required to have a U.S. taxpayer identification number but are not eligible to obtain an SSN. Issued by the IRS.

If the name and TIN on a 1099 do not match IRS records, the payer may receive a CP2100 or CP2100A notice from the IRS. This notice instructs the payer to begin backup withholding on future payments until the payee provides corrected information.

Backup Withholding Rules Explained

Backup withholding is a tax mechanism the IRS uses to ensure that income taxes are collected on certain payments when the recipient's taxpayer information is missing, incorrect, or flagged by the IRS. According to IRS rules, backup withholding requires the payer to withhold a flat percentage from reportable payments and remit that amount directly to the IRS.

Current Backup Withholding Rate: 24%

The current backup withholding rate is 24% of the reportable payment. This rate applies to most 1099-reportable payments when backup withholding is triggered.

Backup withholding is triggered in the following situations:

- Missing TIN: The payee does not provide a Taxpayer Identification Number on Form W-9.

- Incorrect TIN: The IRS notifies the payer that the TIN provided does not match its records.

- IRS Notification: The IRS directly instructs the payer to begin backup withholding on a specific payee due to underreporting of income in prior years.

- Missing Certification: The payee fails to certify on Form W-9 that they are not subject to backup withholding.

When backup withholding applies, the payer must withhold 24% from each payment until the situation is resolved. The withheld amounts are reported on Form 945, Annual Return of Withheld Federal Income Tax, and also shown on the 1099 form issued to the payee. The payee can claim the withheld amount as a credit on their income tax return.

The IRS reminds taxpayers that backup withholding thresholds do not affect whether income is taxable. All income remains taxable regardless of whether backup withholding applies. For third-party settlement organizations, the proposed regulations provide that backup withholding generally is not required unless the gross amount of reportable payment transactions exceeds $20,000 and the number of transactions exceeds 200.

1099 vs W-2 Differences

One of the most common areas of confusion is the difference between Form 1099 and Form W-2. Both forms report income, but they apply to completely different working relationships and have distinct tax implications.

| Feature | Form W-2 (Employee) | Form 1099-NEC (Independent Contractor) |

|---|---|---|

| Worker Classification | Employee | Independent contractor, freelancer, or gig worker |

| Tax Withholding | Employer withholds federal income tax, Social Security, and Medicare | No taxes withheld (unless backup withholding applies) |

| Social Security and Medicare | Employer pays half; employee pays half (7.65% each) | Worker pays both halves as self-employment tax (15.3%) |

| Benefits | May include health insurance, retirement plan, paid time off | No employer-provided benefits |

| Control Over Work | Employer controls how, when, and where work is performed | Contractor controls how the work is accomplished |

| Tax Forms Filed | Form 1040 with W-2 income reported as wages | Form 1040 with Schedule C and Schedule SE |

| Expense Deductions | Limited; unreimbursed employee expenses generally not deductible | Can deduct ordinary and necessary business expenses on Schedule C |

Worker classification matters a great deal. Misclassifying an employee as an independent contractor can result in significant IRS penalties, including back taxes, interest, and fines. The IRS uses several factors to determine worker status, including behavioral control, financial control, and the nature of the relationship. If you are unsure about classification, the IRS provides Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding, which can be used to request an official determination.

Common 1099 Mistakes to Avoid

Both payers and recipients make mistakes with 1099 forms that can lead to IRS notices, penalties, and unnecessary stress. Here are the most frequent errors and how to avoid them:

Wrong TIN or Name Mismatch

This is the most common 1099 error. The name and TIN on the 1099 must match IRS records exactly. Even a small typo can trigger a CP2100 notice. Always verify information against a current Form W-9.

Using the Wrong Form

Nonemployee compensation must be reported on Form 1099-NEC, not Form 1099-MISC. Rents, royalties, and other miscellaneous payments go on Form 1099-MISC. Filing on the wrong form creates confusion and may trigger IRS correspondence.

Missing the Filing Deadline

Form 1099-NEC has a strict January 31 deadline for both recipient copies and IRS filing. No automatic extension is available. Late filing triggers penalties starting at $60 per form.

Failing to Report All Income as a Recipient

Even if you do not receive a 1099 from a payer, you are still legally required to report all taxable income. The IRS matching program will flag discrepancies between your return and payer-reported amounts.

Issuing 1099s to Corporations Unnecessarily

Generally, payments to corporations (except for medical and legal services) do not require a 1099. Issuing unnecessary 1099s creates administrative burden and confusion.

Not Correcting Errors Promptly

If you discover an error on a 1099 you issued, file a corrected form as soon as possible. There are two types of corrections: Type 1 (original was not filed or incorrect payer/recipient info) and Type 2 (incorrect dollar amounts). Each requires a specific correction procedure.

Received an Incorrect 1099? If you receive a 1099 with wrong information, contact the payer immediately. Ask them to issue a corrected form before they file with the IRS. If the payer has already filed, they must submit a corrected form. Keep records of all correspondence in case you need to explain the discrepancy on your tax return.

Can You Receive a 1099 Electronically?

Yes, 1099 forms can be furnished electronically. The IRS allows payers to provide 1099 forms to recipients electronically if the recipient has affirmatively consented to electronic delivery. This consent must be obtained before electronic delivery can be used, and the payer must meet specific IRS requirements regarding the format and accessibility of electronic statements.

For payers, electronic filing with the IRS is required if they file 10 or more information returns in the aggregate during a calendar year. Beginning with the 2026 tax year (filing season 2027), the IRS has transitioned from the legacy Filing Information Returns Electronically (FIRE) system to the modern Information Returns Intake System (IRIS). IRIS is now the only intake system for information returns. The IRS recommends e-filing for all filers, as it is faster, more accurate, and provides immediate confirmation of receipt.

The electronic filing deadline for most 1099 forms (except 1099-NEC) is March 31. Form 1099-NEC must be e-filed by January 31, the same as the paper filing deadline.

Download Official IRS Form 1099-MISC

You can download the official Form 1099-MISC directly from the IRS website. This PDF includes Copy A (for IRS filing), Copy 1 (for state tax department), Copy B (for recipient), and Copy 2 (for recipient's state return).

Download Form 1099-MISC (IRS.gov)Important: Copy A printed from this PDF is not scannable by the IRS. To file with the IRS, you must order official printed forms or e-file through IRIS. Copy B and other copies printed in black are acceptable for furnishing to recipients. Always review the official IRS instructions before completing any tax form.

How Freelancers and Contractors Use 1099 Forms for Tax Reporting

If you work as a freelancer, independent contractor, or gig worker, the 1099-NEC form is central to your tax reporting. Understanding how to use it correctly can save you money and help you avoid IRS problems.

According to the IRS, independent contractors are considered self-employed. They must report their income on Schedule C (Form 1040), Profit or Loss from Business. If net earnings from self-employment are $400 or more, they must also file Schedule SE (Form 1040), Self-Employment Tax. Here is a practical walkthrough of how a freelancer should handle 1099 forms:

Step 1: Collect All 1099 Forms

By early February, you should have received a 1099-NEC from each client that paid you $600 or more (or $2,000 starting in tax year 2026). You may also receive 1099-K forms from payment processors like PayPal or Venmo if your transactions exceeded the reporting threshold.

Step 2: Reconcile Against Your Own Records

Compare the amounts on each 1099 against your own income records. The 1099 amount should match the total payments you received from that client during the year. If it does not, contact the client to resolve the discrepancy.

Step 3: Report Total Gross Income on Schedule C

Report your total gross receipts on Schedule C, line 1. This includes all 1099-reported income plus any income from clients who did not send you a 1099. Even if a client paid you less than the threshold and did not issue a 1099, that income is still taxable and must be reported.

Step 4: Deduct Business Expenses

One major advantage of being self-employed is the ability to deduct ordinary and necessary business expenses. These might include home office expenses, equipment, software subscriptions, travel, marketing, professional services, and health insurance premiums. These deductions reduce your taxable income and your self-employment tax.

Step 5: Calculate Self-Employment Tax on Schedule SE

Self-employment tax covers Social Security and Medicare contributions. The rate is 15.3% on the first portion of your net earnings (12.4% for Social Security and 2.9% for Medicare). You can deduct half of your self-employment tax as an adjustment to income on your Form 1040.

Step 6: Make Quarterly Estimated Tax Payments

Since no taxes are withheld from your 1099 income, you are generally required to make quarterly estimated tax payments to cover both income tax and self-employment tax. The due dates are April 15, June 15, September 15, and January 15 of the following year.

Scam Alert: The IRS warns taxpayers to be vigilant about tax scams involving Form 1099. Fraudsters may send fake 1099 forms to steal personal information or trick recipients into making payments. The IRS will never initiate contact by phone, email, text, or social media to request personal or financial information. If you receive a suspicious 1099, verify it directly with the supposed payer using contact information you find independently, not the information printed on the suspicious form.

Calculate Your Estimated Take-Home Pay Instantly

Wondering how much you will actually keep after self-employment taxes, federal income tax, and state taxes? Try the free paycheck calculator to see your estimated take-home pay and plan your finances with confidence.

Use the Salary After Taxes CalculatorHelpful Tools for Tax Season

While managing your 1099 forms and tax reporting, you may find these free resources useful. FreeAiden offers free AI-powered tools including QR code generators, barcode generators, PDF converters, image tools, and productivity utilities that can help streamline your tax document management workflow. Organizing receipts, converting scanned expense documents, and generating barcodes for your filing system are just a few ways these tools can simplify your tax preparation process.

What Is an IRS 1099 Form? – FAQs

Who receives a 1099 form?

Anyone who receives certain types of non-wage income may receive a 1099 form. This includes independent contractors and freelancers who earned $600 or more (or $2,000 starting in 2026), landlords who collected rent, investors who earned interest or dividends, individuals who sold securities, retirees who took retirement distributions, and people who received unemployment benefits. The specific 1099 variant depends on the income type.

Is a 1099 required for freelancers?

Yes, businesses are generally required to issue Form 1099-NEC to any freelancer or independent contractor to whom they paid $600 or more during the tax year (or $2,000 starting in tax year 2026). However, even if a client does not send you a 1099, you must still report all freelance income on your tax return. The reporting obligation belongs to both the payer and the recipient.

What happens if my 1099 information is wrong?

If you receive a 1099 with incorrect information, contact the payer immediately and request a corrected form. If the payer has already filed the incorrect form with the IRS, they must submit a corrected 1099. If you cannot obtain a correction in time to file your tax return, report the correct income amount on your return and attach an explanation of the discrepancy. Keep documentation to support your position.

What is backup withholding?

Backup withholding is a tax mechanism that requires payers to withhold 24% from reportable payments when the recipient has not provided a valid Taxpayer Identification Number, when the IRS notifies the payer that the TIN is incorrect, or when the IRS instructs withholding due to prior underreporting. The withheld amount is remitted to the IRS and credited to the recipient's tax account. Backup withholding ensures that taxes are collected on payments where the recipient's identity or tax compliance is in question.

Is Form 1099 sent to the IRS?

Yes. When a business issues a 1099 form, it sends Copy A to the IRS and Copy B to the recipient. The IRS uses the information on Copy A to match against the income reported on the recipient's tax return. If there is a discrepancy, the IRS may send a notice, conduct an audit, or assess additional taxes, penalties, and interest. This matching program is a core component of IRS tax compliance enforcement.

Can businesses store 1099 forms electronically?

Yes. Businesses can store 1099 forms electronically, and the IRS encourages electronic recordkeeping. Payers may furnish 1099 forms to recipients electronically if the recipient affirmatively consents. For IRS filing, businesses that file 10 or more information returns in the aggregate must e-file through the IRS Information Returns Intake System (IRIS). Electronic filing is faster, more secure, and provides immediate confirmation.

What is the difference between a 1099 and W-2?

The key difference is employment status. A W-2 is issued to employees, with taxes already withheld by the employer for federal income tax, Social Security, and Medicare. A 1099-NEC is issued to independent contractors and freelancers, with no taxes withheld. Contractors must pay self-employment tax (15.3% for Social Security and Medicare) on their net earnings and make quarterly estimated tax payments. Contractors can also deduct business expenses, which employees generally cannot.

Do I need a W-9 before issuing a 1099?

Yes, it is best practice and strongly recommended to obtain a completed Form W-9 from every vendor or contractor before making any payments. The W-9 provides the legal name, Taxpayer Identification Number, and business classification needed to prepare an accurate 1099. Without a W-9, you risk filing a 1099 with incorrect information, which can trigger IRS notices and penalties. Collect W-9s during onboarding, not at year-end.

What happens if I do not report 1099 income?

If you fail to report income shown on a 1099 form, the IRS matching program will likely detect the discrepancy. You may receive a CP2000 notice proposing additional tax, penalties, and interest. Penalties can include a 20% accuracy-related penalty on the underpayment. In cases of substantial understatement or fraud, higher penalties and even criminal charges are possible. It is always best to report all income accurately and on time.

Do freelancers always receive a 1099?

Not always. A business is required to issue a 1099-NEC only if it paid a freelancer or contractor $600 or more during the tax year (or $2,000 starting in tax year 2026). If your total payments from a particular client were below the threshold, the client is generally not required to issue a 1099. However, you must still report all income you earned, including amounts below the threshold. Also, payments made to corporations generally do not require a 1099, with some exceptions.

Disclaimer

This article is intended for educational and informational purposes only. It does not constitute legal advice, tax advice, or professional financial advice. Tax laws and IRS regulations are subject to change and may vary based on individual circumstances. Every tax situation is different. Before making any decisions or taking any actions based on the information in this article, you should consult directly with a qualified tax professional, certified public accountant, or tax attorney. You should also verify all information against the latest official guidance published by the Internal Revenue Service at www.irs.gov. The author and publisher of this article are not responsible for any errors, omissions, or outcomes resulting from the use of this information.

Final Thoughts

Understanding what an IRS 1099 form is and how it works is an essential skill for anyone who earns income outside of traditional employment. Whether you are a freelancer receiving a 1099-NEC, a landlord receiving a 1099-MISC, or an investor receiving a 1099-INT or 1099-B, the core principle is the same: the IRS knows about this income, and you must report it accurately on your tax return.

The most important takeaways about Form 1099 are straightforward. First, always provide a complete and accurate Form W-9 to every client or payer before they pay you. Second, track your income independently throughout the year so you can verify the accuracy of the 1099 forms you receive. Third, report all income on your tax return, even if you do not receive a 1099 for it. Fourth, take advantage of the business expense deductions available to self-employed individuals to reduce your taxable income legitimately. Fifth, make quarterly estimated tax payments to avoid underpayment penalties and a large tax bill in April.

The 1099 system exists to promote tax compliance and fairness. When everyone reports their income correctly, the tax system works as intended. By understanding how IRS Form 1099 operates, you protect yourself from IRS notices and penalties while fulfilling your tax obligations with confidence.

If you are self-employed or receive 1099 income, take a moment to calculate your take-home pay after accounting for self-employment taxes, federal income tax, and state taxes. Knowing your numbers ahead of time makes tax season far less stressful.

Plan Ahead for Tax Season

Use the free paycheck calculator to estimate your take-home pay, understand your tax obligations, and make smarter financial decisions throughout the year.

Calculate Your Salary After Taxes