Form 1040-NR: What It Is and How to Fill It Out (2026 Guide)

If you earned income from U.S. sources but are not a U.S. citizen or permanent resident, you may need to file Form 1040-NR. This is the official IRS tax return for nonresident aliens. It reports your U.S. income, calculates your tax liability, and determines whether you are owed a refund. Many international students, scholars, temporary workers, and foreign investors use Form 1040-NR as their starting point every tax season. Getting the details right matters because nonresident tax rules differ significantly from the rules that apply to U.S. residents and citizens.

🔹 2026 Updates and Important Notes

- 2026 Form 1040-NR: The IRS has not yet released the 2026 Form 1040-NR (for Tax Year 2025) as of June 11, 2026. This guide is based on the 2025 rules and will be updated once the official 2026 form is published. Always download the latest version from IRS.gov.

- Form 1040-ES (NR) Updates: The 2026 Estimated Tax Worksheet for Nonresidents (Form 1040-ES (NR)) was updated on February 10, 2026, with a new line for additional deductions on Schedule 1-A (Form 1040), line 38.

- ITIN Expiration: Individual Taxpayer Identification Numbers (ITINs) expire if not used on a federal tax return for 3 consecutive years. Check your ITIN status here.

- Belarus Treaty Suspension: The U.S. has partially suspended Article III(1)(g) of the 1973 U.S.-USSR tax convention for Belarus through December 31, 2026.

- Form 8843 Deadline: All F-1, J-1, and M-1 visa holders must file Form 8843 by June 15, 2026, even if they had no U.S. income.

- Dual-Status Aliens: If your tax status changed during 2026 (e.g., from nonresident to resident), you may need to file a dual-status return. These returns cannot be e-filed and must be mailed to the IRS.

- State Taxes: Some states (e.g., California, New York) require nonresidents to file state tax returns if they earned income there. Check your state's rules.

Table of Contents

- What Is Form 1040-NR?

- Who Must File Form 1040-NR?

- Who Does Not Need to File Form 1040-NR?

- When Is Form 1040-NR Required?

- Form 1040-NR Filing Deadlines for 2026

- How to Fill Out Form 1040-NR Step-by-Step

- Line-by-Line Form 1040-NR Instructions

- Types of Income Reported on Form 1040-NR

- Deductions and Credits for Nonresident Aliens

- Tax Treaty Benefits Explained

- Form 1040-NR vs Form 1040

- How International Students and Scholars Use Form 1040-NR

- Form 8843: Required for All F-1, J-1, and M-1 Visa Holders

- Electronic Filing and Mailing Options

- Common Form 1040-NR Mistakes to Avoid

- Form 1040-NR: FAQs

- Filing Form 1040-NR With Confidence

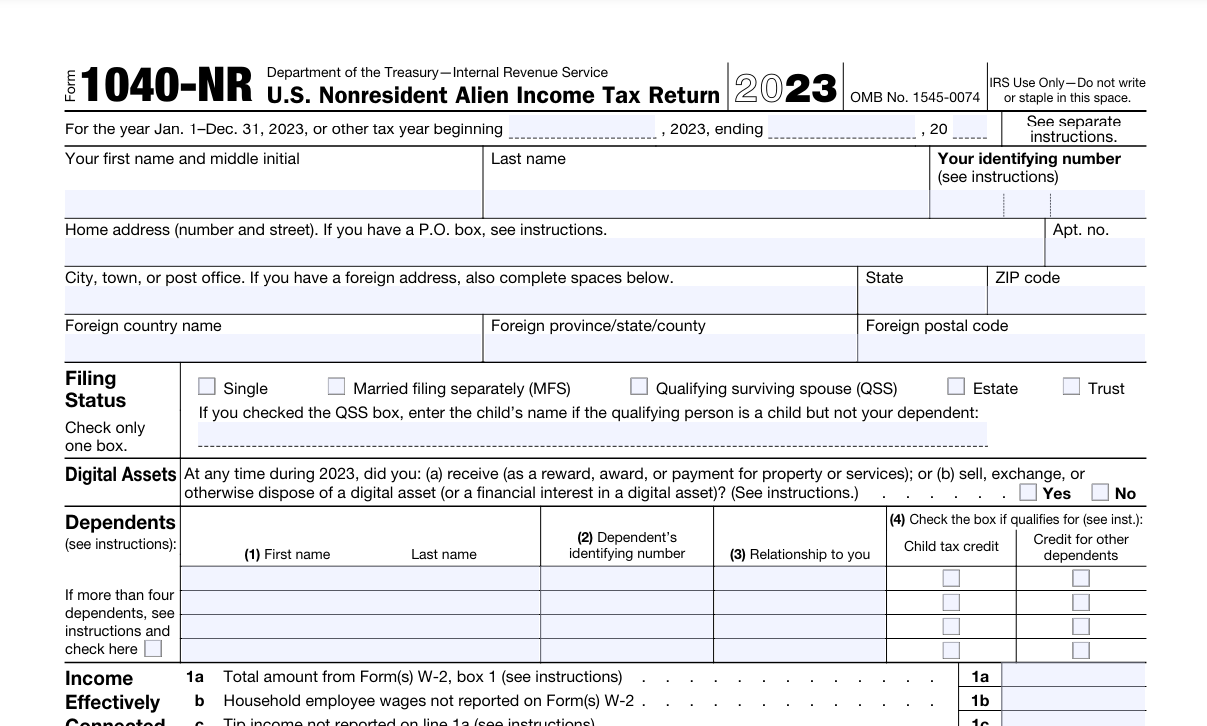

What Is Form 1040-NR?

Form 1040-NR, officially titled "U.S. Nonresident Alien Income Tax Return," is the document the Internal Revenue Service requires nonresident aliens to use when reporting income from U.S. sources. This form calculates your total U.S. tax obligation for a given tax year. It covers wages, tips, scholarship and fellowship grants, investment income, rental earnings, and business income connected to U.S. trade or business activities.

According to IRS guidance, a nonresident alien is anyone who is neither a U.S. citizen nor a U.S. resident for tax purposes. The substantial presence test determines whether someone qualifies as a resident alien. If you do not meet the substantial presence threshold and are not a green card holder, you likely file Form 1040-NR rather than the standard Form 1040.

This guide is based on official IRS Form 1040-NR instructions and educational tax resources. Always download the latest version directly from IRS.gov before you begin preparing your return.

Who Must File Form 1040-NR?

You must file Form 1040-NR if you are a nonresident alien engaged in a U.S. trade or business during the tax year, even if you had no income from that trade or business. You also must file if you have U.S. source income and not all of the tax owed was withheld by a payer. Common groups who file this form include:

- International students on F-1, J-1, or M-1 visas who have U.S. scholarships, fellowships, or employment income.

- Temporary workers on H-1B, TN, or O-1 visas during their first years in the U.S., before meeting the substantial presence test.

- Foreign investors who earn dividends, interest, or rental income from U.S. properties.

- Artists, athletes, and entertainers who perform in the U.S. and receive payment from U.S. sources.

- Nonresident aliens who sold U.S. real estate and need to report the gain or loss.

If you had any U.S. source income and you are not certain whether you qualify as a resident or nonresident for tax purposes, the IRS substantial presence test calculator on IRS.gov can help you determine your correct filing status. Filing the wrong form can delay your refund and trigger IRS correspondence.

Who Does Not Need to File Form 1040-NR?

Not every nonresident alien with U.S. connections needs to file. You may not need to file Form 1040-NR if your only U.S. source income is from interest and dividends that are not effectively connected with a U.S. trade or business, and the correct withholding was applied at the source. Additionally, if your only U.S. income is from wages that did not exceed the personal exemption amount (when applicable under a tax treaty), filing may not be required. However, filing a return is the only way to claim a refund of over-withheld taxes, so many nonresident aliens benefit from filing even when not strictly required.

When Is Form 1040-NR Required?

Form 1040-NR is required for any tax year in which a nonresident alien has income that is subject to U.S. tax and the tax was not fully satisfied through withholding. The form becomes necessary when you have effectively connected income, FDAP income (fixed, determinable, annual, or periodic), or both. Even if a tax treaty reduces your rate to zero, you must still file the form to claim the treaty benefit and document the exemption.

Form 1040-NR Filing Deadlines for 2026

The standard filing deadline for Tax Year 2025 (filed in 2026) is April 15, 2026. If you did not receive wages subject to U.S. withholding, the deadline extends to June 15, 2026. Taxpayers who need more time can file Form 4868 to request an automatic extension. The extension gives you until October 15, 2026 to submit your return, but it does not extend the time to pay any tax owed. Interest accrues on unpaid balances from the original due date. According to IRS guidance, paying as much as you can by the original deadline minimizes interest charges.

Note for F-1/J-1 Students: If you were in the U.S. on an F-1, J-1, or M-1 visa for any part of 2025, you must file Form 8843 by June 15, 2026, even if you had no U.S. income. If you also had taxable U.S. income, you must file Form 1040-NR by April 15, 2026.

How to Fill Out Form 1040-NR Step-by-Step

Filling out Form 1040-NR correctly requires gathering all relevant income documents before you start. You will need Forms W-2, 1042-S, 1099, and records of any tax treaty claims. The form has several parts, and each section builds on the previous one. Taking a systematic approach reduces errors and helps you claim every deduction and credit you qualify for.

Line-by-Line Form 1040-NR Instructions

Each section of Form 1040-NR serves a distinct purpose. Understanding what goes where prevents mistakes that could cost you money or trigger an IRS notice. Below is a practical walkthrough of the major parts of the form.

Part I — Identification

Enter your full legal name, your Individual Taxpayer Identification Number (ITIN) or Social Security Number (SSN), and your current mailing address. If you are filing jointly (allowed only for certain married nonresident aliens from Canada, Mexico, South Korea, or those with a U.S. citizen spouse who elect to file jointly), include spouse information. Most nonresident aliens file as "Single" or "Married filing separately."

Part II — Income

Report all U.S. source income here. Wages go on the designated wage line. Taxable scholarships and fellowships are also reported. Interest and dividends appear on separate lines. Effectively connected business income flows from Schedule C if you operated a U.S. business. Capital gains from U.S. real estate or securities go on the appropriate lines as directed by the IRS instructions.

Part III — Tax and Credits

This section calculates your tax using either the graduated rate tables (for effectively connected income) or the flat 30% rate (for FDAP income not reduced by treaty). If a tax treaty reduces your rate, you enter the treaty-based reduction here. The foreign tax credit may also be available if you paid taxes to another country on the same income.

Part IV — Payments

Enter all federal income tax withheld, as shown on your W-2 and 1042-S forms. Include any estimated tax payments you made during the year and any amount paid with an extension request. This section determines whether you have already satisfied your tax obligation.

Part V — Refund or Amount You Owe

If your payments exceed your tax, you will see a refund amount. If your tax exceeds payments, you will owe the difference. The IRS offers direct deposit for refunds to U.S. bank accounts. For amounts owed, payment options include IRS Direct Pay, credit card, or a check mailed with the return.

Schedule OI — Other Information

Schedule OI is mandatory for most nonresident filers. You must disclose your visa type, the number of days you were present in the U.S., your country of residence, and any tax treaty positions you are claiming. Complete this schedule carefully. Incomplete Schedule OI entries are a common reason for IRS processing delays.

Types of Income Reported on Form 1040-NR

Nonresident aliens must report two broad categories of U.S. source income: effectively connected income and FDAP income. The distinction matters because each category faces different tax rates and rules.

| Income Type | Tax Treatment | Common Examples |

|---|---|---|

| Effectively Connected Income (ECI) | Taxed at graduated U.S. rates after allowable deductions | U.S. wages, self-employment income from a U.S. business, rental income with a net election |

| Fixed, Determinable, Annual, or Periodic (FDAP) Income | Taxed at a flat 30% rate unless a treaty reduces it | Interest, dividends, royalties, certain scholarship amounts, rents not connected to a U.S. business |

Some income can fall into both categories depending on facts and circumstances. For example, rental income is normally FDAP but can become ECI if you make a special election with the IRS. Always check the IRS instructions for Form 1040-NR to classify your income correctly.

Deductions and Credits for Nonresident Aliens

Deductions for nonresident aliens are more limited than for U.S. residents. Generally, you cannot claim the standard deduction unless you are a student or apprentice from India eligible under the U.S.-India tax treaty. Most nonresident aliens itemize deductions related to effectively connected income. Allowable itemized deductions include state and local income taxes, charitable contributions to U.S. qualified organizations, and certain casualty losses. Business expenses connected to U.S. trade or business activities are also deductible on Schedule C.

Credits available to eligible nonresident aliens include the foreign tax credit, which prevents double taxation when another country also taxes the same U.S. source income. Some nonresident aliens from Canada, Mexico, South Korea, or India may qualify for the child tax credit or the additional child tax credit for qualifying dependent children. The earned income credit is generally not available to nonresident aliens.

Tax Treaty Benefits Explained

The United States maintains income tax treaties with over 60 countries. These treaties often reduce or eliminate U.S. tax on certain types of income for qualifying residents of treaty partner countries. Common treaty benefits include reduced withholding rates on dividends and interest, exemption for scholarship and fellowship grants, and exclusion of certain wages earned by students and researchers. To claim a treaty benefit, you must file Form 1040-NR and disclose the treaty position on Schedule OI. You must also have a valid ITIN or SSN. According to IRS guidance, failing to properly disclose a treaty claim can result in the benefit being disallowed.

2026 Treaty Updates: The U.S. has partially suspended Article III(1)(g) of the 1973 U.S.-USSR tax convention for Belarus through December 31, 2026. The U.S. has no income tax treaties with Argentina, Brazil, Saudi Arabia, the UAE, or Singapore as of 2026. The U.S.-India treaty still allows Indian students to claim the standard deduction.

Form 1040-NR vs Form 1040

Form 1040-NR and Form 1040 serve different taxpayer populations and have important structural differences. The table below highlights the key distinctions.

| Feature | Form 1040-NR | Form 1040 |

|---|---|---|

| Who uses it | Nonresident aliens | U.S. citizens and resident aliens |

| Standard deduction | Generally not available (exception for India treaty) | Available to most filers |

| FDAP income | Separately reported, flat 30% rate | Not applicable |

| Tax treaty claims | Common, reported on Schedule OI | Rare |

| Filing status options | Limited; generally Single or Married Filing Separately | Multiple options including Head of Household |

How International Students and Scholars Use Form 1040-NR

International students on F-1 or J-1 visas and scholars on J-1 visas are among the most frequent filers of Form 1040-NR. During their first five calendar years in the U.S., F-1 and J-1 students are generally considered nonresident aliens for tax purposes. J-1 scholars typically remain nonresident for two out of the past six years. During these nonresident years, they file Form 1040-NR. Wages from on-campus employment, assistantships, and practical training are reported as effectively connected income. Scholarship and fellowship grants that exceed qualified tuition and required fees are taxable and must be reported. Many students benefit from tax treaty provisions that exempt a portion of their earnings. Filing correctly protects visa status and builds a clean tax record in the U.S.

FICA Exemption: F-1, J-1, and M-1 students are exempt from Social Security and Medicare taxes (FICA) if employed on-campus or under a treaty. Non-students (e.g., H-1B, TN) may owe FICA taxes unless exempt by treaty. Use Form 8233 to claim treaty exemptions for wages.

Form 8843: Required for All F-1, J-1, and M-1 Visa Holders

Form 8843 is a required form for all F-1, J-1, and M-1 visa holders, even if they had no U.S. income. This form helps the IRS determine your tax residency status and ensures compliance with U.S. tax laws. The deadline for filing Form 8843 is June 15, 2026 for Tax Year 2025.

If you also had U.S. source income, you must file both Form 8843 and Form 1040-NR by their respective deadlines (April 15 for Form 1040-NR, June 15 for Form 8843). Failure to file Form 8843 can result in penalties and may affect your visa status.

Download Form 8843

Review official IRS instructions before filing.

Curious how much of your paycheck you actually keep after taxes? Use our free tool to calculate your take-home pay.

Calculate Your Estimated Take-Home PayElectronic Filing and Mailing Options

Form 1040-NR can be e-filed through certain IRS-approved software providers that support nonresident returns. E-filing reduces errors through built-in checks and speeds up refund processing. If you prefer to file on paper, you must mail your completed return to the IRS address specified in the Form 1040-NR instructions. The mailing address depends on whether you are enclosing a payment or expecting a refund. Always use certified mail or a delivery service with tracking when mailing tax documents to the IRS. Keep copies of everything you send for your records.

Dual-Status Aliens: If your tax status changed during 2026 (e.g., from nonresident to resident), you cannot e-file your return. You must mail a dual-status return to the IRS. Refer to IRS Publication 519 for guidance.

Download Form 1040-NR

Review official IRS Form 1040-NR instructions before filing.

Common Form 1040-NR Mistakes to Avoid

Even small errors on Form 1040-NR can cause processing delays, rejected refund claims, or IRS notices. Below are mistakes the IRS frequently sees on nonresident returns and how to avoid them.

- Filing Form 1040 instead of Form 1040-NR. If you are a nonresident alien, using the wrong form can invalidate your return and delay any refund.

- Skipping Schedule OI. The IRS uses Schedule OI to verify your nonresident status and treaty claims. An incomplete Schedule OI is a top reason for processing holds.

- Claiming the standard deduction without treaty eligibility. Most nonresident aliens cannot claim the standard deduction. Only those eligible under specific treaties (such as the India treaty) should claim it.

- Misclassifying income. FDAP income and effectively connected income have different tax rates and reporting lines. Mixing them up leads to incorrect tax calculations.

- Missing ITIN or SSN. Every Form 1040-NR must include a valid taxpayer identification number. If you do not have an SSN, apply for an ITIN using Form W-7 well before the filing deadline.

- Forgetting to sign and date the return. An unsigned return is not valid and will be returned by the IRS.

- Not filing Form 8843 (if applicable). F-1, J-1, and M-1 visa holders must file Form 8843 by June 15, even if they had no U.S. income.

Important: If you discover an error after filing, you can correct it by filing Form 1040-X, the amended U.S. individual income tax return. Nonresident aliens who originally filed Form 1040-NR should use Form 1040-X and clearly mark the amended return. Keep copies of all amended filings and supporting documentation for at least three years from the original filing date.

Form 1040-NR: FAQs

Filing Form 1040-NR With Confidence

Filing a U.S. tax return as a nonresident alien does not need to feel overwhelming. Start by confirming your tax status using the IRS substantial presence test. Gather every income document you received, including those from foreign payers that relate to U.S. source income. Identify which income is effectively connected and which falls under FDAP rules. If a tax treaty applies, confirm your country of residence is a treaty partner and that you meet all conditions for the benefit.

Complete Schedule OI with accurate information about your visa, days of presence, and treaty position. Fill out each part of Form 1040-NR in order, double-checking that amounts from your income documents match the figures you enter. Don't forget to file Form 8843 by June 15, 2026 if you are an F-1, J-1, or M-1 visa holder. Sign the return and attach all required schedules. If you owe tax, pay by the deadline to minimize interest. If you are owed a refund, choose direct deposit for the fastest receipt.

Many nonresident taxpayers also find it helpful to use a paycheck calculator to estimate their take-home pay during the year so there are fewer surprises at tax time. Understanding your salary after taxes can help you plan for any tax bill that may arise when you file. For those who want to double-check their work, free tools exist online, including resources at freeaiden.com, that can help you organize tax information before submitting your return.

When you take the time to understand the rules and follow the IRS instructions, you can file Form 1040-NR accurately and with confidence. A correct return protects your immigration status, builds a positive U.S. tax history, and ensures you receive any refund you are entitled to without unnecessary delay.

Ready to estimate your take-home pay? Use our free paycheck calculator to see how taxes affect your earnings.

Calculate Your Take-Home Pay Now