Schedule C: Profit or Loss From Business Explained

If you work for yourself, understanding Schedule C: Profit or Loss From Business Explained is the gateway to reporting your income correctly and paying only the tax you owe. This form is where sole proprietors and single-member LLC owners show the IRS how much money their business made and which expenses kept the operation running. Getting it right protects your hard-earned profit and keeps your tax record clean.

This guide walks you through every important part of Schedule C using official IRS guidance — from who files it to how to claim deductions like home office and vehicle costs. You will learn what counts as business income, how to calculate net profit, and how Schedule C connects to your self-employment tax. Our goal is to turn an intimidating IRS form into a straightforward tool you can handle with confidence.

This guide is based on official IRS Schedule C instructions and educational tax resources.

Table of Contents

- What Is IRS Schedule C?

- Who Must File Schedule C?

- Who Does Not Need Schedule C?

- When Is Schedule C Required?

- Business Income Reported on Schedule C

- Business Expenses You Can Deduct

- Schedule C Line-by-Line Instructions

- Cost of Goods Sold

- Vehicle Expenses

- Home Office Deduction

- Depreciation

- Inventory

- Gross Profit vs Net Profit

- Schedule C and Self-Employment Tax

- Schedule C and Schedule SE

- Schedule C for Sole Proprietors

- Schedule C for Single-Member LLCs

- Estimated Taxes

- Recordkeeping Requirements

- Common Schedule C Mistakes

- How to File Schedule C Electronically

- Schedule C FAQs

- Getting Schedule C Right

What Is IRS Schedule C?

IRS Schedule C is the form you attach to your annual Form 1040 to tell the IRS about your business profit or loss. Think of it as a mini income statement designed specifically for self-employed individuals. The form tallies all the money your business brought in and subtracts the costs you paid to keep it running. The resulting number — net profit or loss — flows directly to your personal tax return.

According to IRS guidance, Schedule C is used by sole proprietors and by single-member limited liability companies (LLCs) that are considered disregarded entities for tax purposes. Even if you have a full-time job and run a small weekend business, you still need to file this form for that side activity. The IRS wants to see every dollar earned, but they also allow you to claim legitimate business expenses that reduce your taxable income.

What makes Schedule C so important is that it determines not just your income tax but also your self-employment tax. That’s the Social Security and Medicare contribution you pay when you don’t have an employer withholding those taxes from your paycheck. Understanding the form helps you plan for that extra tax bite and avoid surprises.

Who Must File Schedule C?

You must file Schedule C if you carried on a trade or business as a sole proprietor and your activity was engaged in for profit. The IRS defines a business broadly: freelancers, gig workers, independent contractors, rideshare drivers, artisans, consultants, and small shop owners all qualify. Even if you earned only a few thousand dollars, the reporting requirement applies as long as the activity is regular and continuous and you intend to make a profit.

Single-member LLC owners also file Schedule C unless they elected to be taxed as a corporation. The default tax classification for a single-member LLC is a disregarded entity, which simply means the IRS treats you as a sole proprietor for tax purposes. So you’ll use Schedule C exactly the same way a traditional sole proprietor does.

If you operate more than one distinct business, you generally need a separate Schedule C for each. For example, a person who runs a landscaping business and also sells handmade jewelry online would file two Schedule C forms, each with its own income and expenses.

Who Does Not Need Schedule C?

You won’t file Schedule C if your business is structured as a C corporation, S corporation, or partnership. Those entities have their own tax returns (Form 1120, 1120S, or 1065). Also, if your single-member LLC has elected to be taxed as an S corporation, you’d file Form 1120S instead and report your income on Schedule E and wages on Form W-2.

Additionally, if your activity is not for profit — meaning it’s a hobby — you don’t use Schedule C. Hobby income is reported directly on Schedule 1 (Form 1040), and expense deductions are limited. The IRS looks at whether you depend on the income, whether you put in time and effort like a business, and if you have a profit motive.

When Is Schedule C Required?

Schedule C is required any year your business had gross receipts of $400 or more from self-employment activities, or if you had any net profit subject to self-employment tax. The IRS uses the $400 threshold to determine if you owe self-employment tax, but even below that, reporting the income on your return is wise to maintain consistency. You file Schedule C with your Form 1040 by the regular tax deadline — for the 2026 tax year, that’s April 15, 2027. If you request an extension, you’ll still have to pay any taxes owed by the original deadline to avoid penalties.

Business Income Reported on Schedule C

Line 1 of Schedule C asks for gross receipts or sales. This includes all the money you received from your business activities during the year, whether paid in cash, check, credit card, or digital payment apps. It also covers amounts reported to you on Form 1099-NEC or 1099-K. The total must reflect the full amount before any expenses are subtracted.

Other income streams, like interest on business bank accounts, refunds of previously deducted business expenses, or the value of bartered services, also count. If you sold products, your gross receipts feed into the cost of goods sold calculation, which we’ll cover later. Accurate reporting here sets the foundation for your entire return.

Business Expenses You Can Deduct

Deductible business expenses are the ordinary and necessary costs of running your trade. The IRS defines ordinary as common and accepted in your field, and necessary as helpful and appropriate. You don’t have to be profitable to deduct them, but you must have proper records.

Website hosting, business cards, social media ads.

Mileage or actual costs for business driving.

Paper, ink, laptops, and furniture under de minimis safe harbor.

Legal, accounting, and bookkeeping fees.

Office rent, internet, phone, and electricity for business space.

Liability, business property, and health insurance for self-employed.

Many other categories exist, such as travel, meals (generally 50% deductible), education to improve business skills, and depreciation on big-ticket assets. The key is that every deduction must tie directly to your business and be documented.

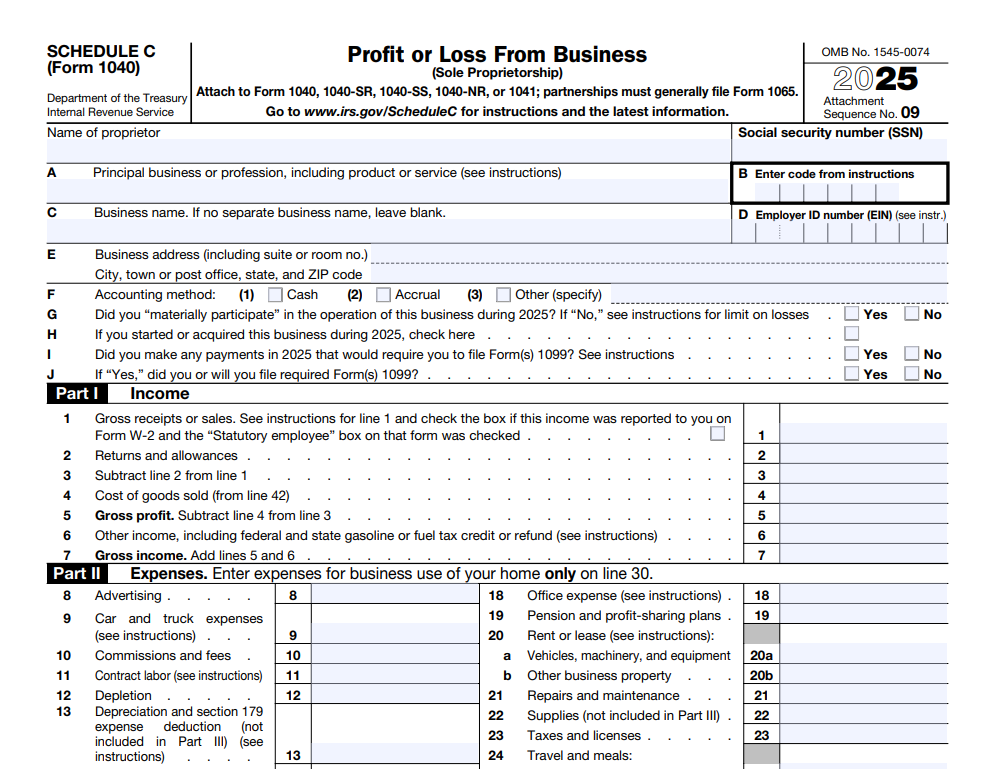

Schedule C Line-by-Line Instructions

While the official IRS instructions give precise details, walking through the core parts of the form helps you understand the flow. The form has five parts: Income, Expenses, Cost of Goods Sold, Information on Your Vehicle, and Other Expenses.

Part I – Income

Line 1: Gross receipts or sales. Enter total revenue before deductions. Line 2: Returns and allowances. Deduct refunds you gave customers. Line 4: Cost of goods sold (from Part III). Subtract COGS to get Line 5: Gross profit. Then add Line 6: Other income, such as interest or fuel tax credits. Line 7: Gross income. This is your total income before operating expenses.

Part II – Expenses

This section lists common expense categories on lines 8 through 27a. You enter amounts for advertising, vehicle expenses, commissions, contract labor, depreciation, insurance, interest, legal fees, office expenses, supplies, travel, meals, utilities, and more. Line 27a: Other expenses is where you list items that don’t fit elsewhere, attaching a statement if needed. Line 28: Total expenses sums everything up.

Line 29: Tentative profit or loss subtracts total expenses from gross income. Line 30: Expenses for business use of your home (from Form 8829). Subtract that to reach Line 31: Net profit or loss. That number goes to your Form 1040 Schedule 1 and Schedule SE.

Cost of Goods Sold

If your business sells products, you must complete Part III. COGS includes the direct costs of the items you sold: beginning inventory, purchases, materials, labor, and other allocable costs, minus ending inventory. This calculation ensures you only deduct the cost of items actually sold, not unsold stock. Even small online sellers need to track inventory if they produce or buy goods for resale. Using a consistent inventory method (cost or lower of cost or market) is required by IRS rules.

Vehicle Expenses

Part IV asks whether you used a vehicle for business. You must answer yes and provide the miles driven for business, commuting, and other personal use. You can choose between the standard mileage rate (set annually by the IRS) or actual expenses like gas, repairs, and depreciation. Your choice in the first year can affect future deductions, so keep thorough records. A mileage log is essential — note the date, destination, purpose, and miles for each trip.

Home Office Deduction

If you use part of your home exclusively and regularly as your principal place of business, you can claim the home office deduction. There are two methods: the simplified option ($5 per square foot up to 300 square feet, maximum $1,500 deduction) and the regular method (actual expenses prorated based on business-use percentage). Form 8829 feeds the deduction to Schedule C, Line 30. The exclusive-use rule is strict; a desk in the living room that doubles as a family TV area won’t qualify.

Depreciation

When you buy equipment, furniture, or vehicles that last more than one year, you generally recover the cost over time through depreciation. Schedule C allows Section 179 expensing (up to a limit) and bonus depreciation to accelerate deductions. Form 4562 calculates depreciation and you enter the total on the appropriate expense line. Not all assets are depreciated the same way, so using IRS tables is important.

Inventory

Businesses that produce, purchase, or sell merchandise must account for inventory at the beginning and end of the year. Proper inventory tracking affects COGS and gross profit. Small taxpayers may qualify for simplified inventory rules, but even then accurate counts and valuation matter. Under IRS rules, you must use a method that clearly reflects income.

Gross Profit vs Net Profit

Gross profit is sales minus cost of goods sold. Net profit, found on Line 31, is what remains after all operating expenses, including home office and depreciation. Net profit is the number that ultimately determines your income tax and self-employment tax. A net loss can offset other income on your 1040, subject to hobby loss rules and at-risk limitations.

Schedule C and Self-Employment Tax

Your net profit from Schedule C isn’t just subject to income tax — it’s also subject to self-employment tax. This tax represents the employer and employee portions of Social Security and Medicare. For 2026, the self-employment tax rate remains 15.3% on the first $168,600 of combined wages and self-employment income (Social Security portion) and 2.9% on all amounts beyond that for Medicare. Half of the self-employment tax is deductible as an adjustment to income on Form 1040.

Schedule C and Schedule SE

Schedule SE (Self-Employment Tax) uses the net profit from Schedule C to compute exactly what you owe. You combine profits from all Schedule C forms if you have more than one business, apply the 92.35% factor, and calculate the tax. Schedule SE must be filed if net earnings from self-employment are $400 or more. The result gets added to your total tax on Form 1040.

Schedule C for Sole Proprietors

For a sole proprietor, Schedule C is your business’s tax identity. There’s no legal separation between you and the business, so all profit flows to your personal return. This simplicity is one reason so many startups begin as sole proprietorships. But remember, without a separate legal entity, your personal assets could be at risk if the business is sued. Even so, tax reporting remains straightforward with Schedule C.

Schedule C for Single-Member LLCs

An LLC with only one owner is automatically a disregarded entity for federal tax purposes. That means you file Schedule C just like any sole proprietor. The LLC provides legal protection but doesn’t change your tax filing unless you elect corporate treatment. So as a single-member LLC owner, you’ll still report income, expenses, and net profit on Schedule C and pay self-employment tax on the profit.

Download the current-year Form 1040 Schedule C directly from the IRS website.

Review the official IRS instructions before filing.

Estimated Taxes

Because no employer withholds taxes from your self-employment income, the IRS requires you to pay estimated taxes quarterly. These cover both income tax and self-employment tax. You calculate estimated payments using Form 1040-ES. Missing payments can lead to underpayment penalties. Using a paycheck calculator to understand withholding equivalents can help you set aside the right amount each quarter.

Recordkeeping Requirements

Good records are the backbone of a solid Schedule C. The IRS expects you to keep receipts, invoices, bank statements, credit card statements, mileage logs, and any documents proving income and deductions. Digital records are acceptable as long as they are clear and accessible. Keep all tax records for at least three years from the date you filed the return, or longer if you claimed a loss carryforward.

Without documentation, the IRS can disallow deductions, increasing your tax bill. A simple spreadsheet or accounting software that categorizes expenses as they appear on Schedule C will save hours of stress later. If you ever face an audit, organized records are your best defense.

Common Schedule C Mistakes

One frequent error is mixing personal and business expenses. Only business costs belong on Schedule C. Another is overstating home office deductions without meeting the exclusive-use test. Many filers forget to report all 1099-NEC income, which the IRS matches with its own records. Also, neglecting to file Schedule SE when profit exceeds $400 can trigger notices. Take your time and double-check each line against your records.

How to File Schedule C Electronically

Most tax software walks you through Schedule C by asking simple questions about your business income and expenses. The software then populates the correct lines and calculates net profit. E-filing is faster, reduces math errors, and gets your refund processed quicker. You can also use IRS Free File if you qualify. When you e-file, the program typically generates Schedule SE and applies the self-employment tax automatically.

Calculate Your Estimated Take-Home Pay

See how self-employment income affects your after-tax earnings with our salary after taxes calculator.

Schedule C: Profit or Loss From Business Explained – FAQs

Any individual operating a business as a sole proprietor or single-member LLC with business income. Even part-time freelancing requires filing if you had profit or want to claim deductions.

Schedule C calculates net business profit. Schedule SE uses that profit to compute self-employment tax, the Social Security and Medicare contribution for self-employed people.

Yes, if the space is used exclusively and regularly for business. The simplified method allows $5 per square foot up to 300 sq ft. The regular method uses actual expenses prorated.

Report the loss; it reduces your total taxable income. The IRS may question losses year after year if they suspect a hobby, so ensure you can demonstrate profit motive.

No. Hobby income goes on Schedule 1. Expenses are limited and can’t exceed income. The distinction hinges on whether you run the activity like a business with profit intent.

Track business miles and choose standard mileage rate or actual expenses. Keep a detailed log. Commuting is personal and not deductible.

Receipts, invoices, bank records, mileage logs, and expense proofs. Maintain them at least 3 years. Digital copies are acceptable.

Schedule C is part of your Form 1040 due April 15. For the 2026 tax year, file by April 15, 2027, unless you have an extension.

Yes, by default a single-member LLC is a disregarded entity and files Schedule C. Only if it elects corporate taxation does it file a different return.

Net profit increases your adjusted gross income and self-employment tax. Deductions lower both. Plan for quarterly estimated payments to avoid a large year-end balance.

Content is reviewed by a financial analyst and IRS tax education researcher to ensure accuracy and clarity. For additional free tax tools and resources, you might explore FreeAiden.com for planning aids.

Getting Schedule C Right

When you sit down to prepare your taxes, approach Schedule C methodically. Start by gathering all income records: 1099 forms, payment processor summaries, and business bank statements. Reconcile every dollar so your Line 1 matches your actual revenue. Then organize expenses into the categories the form provides. If you’re unsure about a deduction, refer back to the IRS instructions or use the search tool on IRS.gov.

Keep in mind that Schedule C is not just a compliance chore — it’s a snapshot of your business health. A rising net profit shows growth, while a legitimate loss might indicate areas to improve. Use this form as a check-in on your pricing, cost control, and overall strategy. Make sure you’re setting aside at least 25-30% of your profit for income and self-employment taxes, and remit estimated payments on time.

Before you file, double-check that you’ve answered the vehicle use questions in Part IV if you claim car expenses, and that your home office deduction flows from Form 8829 if applicable. Review the math and confirm that net profit on Line 31 correctly carries to Schedule 1 and Schedule SE. Finally, keep your documentation organized for at least three years.

Taking the time to understand Schedule C: Profit or Loss From Business Explained puts you in control of your tax situation. You can confidently claim every deduction you’re entitled to while staying fully compliant with IRS rules. Whether you’re a freelancer, gig worker, or small business owner, accurate Schedule C reporting protects your income and supports your financial future.

Use Our Paycheck Calculator to Plan Your Taxes

Get a clear picture of your take-home pay after self-employment tax and deductions.

| Quick Reference | Details |

|---|---|

| Form Name | Schedule C (Form 1040) |

| Who Files | Sole proprietors, single-member LLCs |

| Income Reported | Gross receipts, sales, other business income |

| Key Deductions | Vehicle, home office, supplies, COGS, insurance |

| Tax Impact | Affects income tax and self-employment tax |

| Filing Deadline | April 15, 2027 (for tax year 2026) |