Schedule D (Form 1040): Capital Gains and Losses Explained

Taxpayer reviewing IRS Schedule D to report capital gains and losses.

Filing Schedule D (Form 1040): Capital Gains and Losses Explained is a must whenever you sell stocks, bonds, cryptocurrency, real estate, or other capital assets. The IRS uses this form to calculate your taxable gains and allowable losses. Many people feel unsure about what to report, how to handle carryovers, or why short‑term and long‑term gains are treated so differently. This guide walks you through every part of Schedule D using official IRS instructions, so you can file correctly and avoid costly mistakes.

Table of Contents

- What Is Schedule D?

- Who Must File Schedule D?

- What Are Capital Gains?

- What Are Capital Losses?

- Short‑Term vs Long‑Term Capital Gains

- How Schedule D Works

- Understanding Form 8949

- Reporting Investment Sales

- Capital Loss Deduction Rules

- Capital Loss Carryovers

- Schedule D and Form 1040

- Special Rules for Cryptocurrency

- Common Filing Mistakes

- FAQs

What Is Schedule D (Form 1040): Capital Gains and Losses Explained?

Schedule D is the IRS form where you calculate the net result of all your capital asset transactions during the tax year. It's not filed by itself — it always attaches to your Form 1040. According to IRS guidance, you use Schedule D to figure the overall capital gain or loss after combining short‑term and long‑term results.

The form itself is relatively short, but it pulls numbers from Form 8949, where you list each individual sale. Schedule D then summarizes those totals, applies netting rules, and determines whether you have a net capital gain (which may be taxed at preferential rates) or a net capital loss (which is subject to deduction limits).

Think of Schedule D as the final scorecard for your investment activity. If you sold shares of an ETF, closed a crypto position, or sold a vacation home, those transactions eventually land on this form. The IRS instructions for Schedule D (Form 1040) provide the exact line‑by‑line steps, and this article explains them in plain language.

Who Must File Schedule D?

You generally must file Schedule D if you had any of the following during the tax year:

- Sold or exchanged capital assets such as stocks, bonds, mutual funds, ETFs, or real estate (unless the gain isn't taxable or the transaction is otherwise excluded).

- Received capital gain distributions from a mutual fund or REIT, even if no sale occurred.

- Reported a capital loss carryover from a prior year.

- Had a worthless security or a bad debt treated as a capital loss.

- Received a Form 1099‑B, 1099‑S, or a brokerage statement showing sales of covered or noncovered securities.

However, if your only capital gains are from capital gain distributions that you report directly on Form 1040 without needing Schedule D, you may not need to file it. According to IRS Schedule D instructions, if you meet certain conditions (like no other capital transactions and no loss carryovers), you can report qualified dividends and capital gain distributions on Form 1040 alone. But if you have any sales of assets or a carryover, Schedule D becomes mandatory.

What Are Capital Gains?

A capital gain happens when you sell a capital asset for more than its cost basis. The cost basis is generally what you paid for the asset, including commissions and certain adjustments. For example, if you bought 100 shares of a stock for $5,000 and sold them later for $8,000, you have a $3,000 capital gain.

Capital gains fall into two categories: short‑term (held one year or less) and long‑term (held more than one year). The holding period starts the day after you acquire the asset and ends on the day you sell it. Even a single day difference can change the tax rate dramatically.

According to IRS guidance, almost everything you own and use for personal or investment purposes is a capital asset, including your home, car, furniture, and stocks. But certain property like inventory or business accounts receivable is not a capital asset, so gains from those are ordinary income.

What Are Capital Losses?

A capital loss occurs when you sell a capital asset for less than your adjusted basis. If you purchased cryptocurrency for $2,000 and sold it for $1,200, you have an $800 capital loss. Losses can offset gains dollar for dollar, which is a valuable tax planning tool. The IRS allows you to use capital losses to reduce your taxable income, but with specific limits.

Not all losses are deductible, however. Losses from the sale of personal‑use property (like a personal car sold at a loss) are not deductible. Only losses on investment property or business assets count. And wash sale rules can disallow a loss if you repurchase substantially identical securities within 30 days before or after the sale.

Short‑Term vs Long‑Term Capital Gains

The holding period determines whether a gain is short‑term or long‑term, and the tax rate difference is significant. Short‑term capital gains are taxed as ordinary income, meaning they can be subject to rates as high as 37% in 2026. Long‑term capital gains benefit from reduced tax rates of 0%, 15%, or 20%, depending on your taxable income.

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $47,025 | $47,026 – $518,900 | Over $518,900 |

| Married Filing Jointly | Up to $94,050 | $94,051 – $583,750 | Over $583,750 |

| Head of Household | Up to $63,000 | $63,001 – $551,350 | Over $551,350 |

| Married Filing Separately | Up to $47,025 | $47,026 – $291,850 | Over $291,850 |

*The 3.8% Net Investment Income Tax (NIIT) may also apply on top of these rates for higher‑income taxpayers.

Short‑term losses are first netted against short‑term gains, and long‑term losses against long‑term gains. If the results are of opposite signs, you combine them. This netting order matters because it can preserve the preferential long‑term rate.

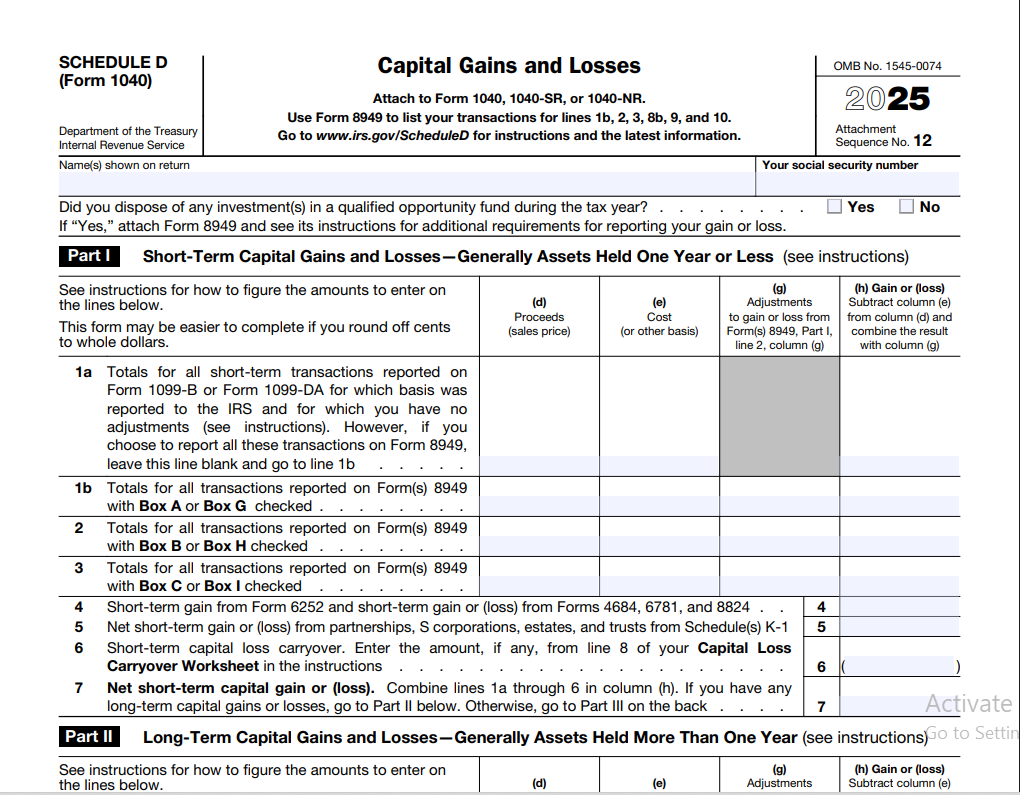

How Schedule D Works

Schedule D has three main parts. Part I handles short‑term capital gains and losses, Part II covers long‑term, and Part III calculates the overall net capital gain or loss and applies special rules like the 28% rate gain or unrecaptured Section 1250 gain for real estate.

Here’s a simplified flow of the Schedule D filing process:

According to IRS instructions, you first complete Form 8949 for each category of transaction (short‑term covered, short‑term noncovered, etc.) and then transfer the subtotals to Schedule D. You do not list individual sales on Schedule D itself.

Need the official form? Download Schedule D (Form 1040) directly from the IRS. Review the official IRS instructions before completing your return.

Download Schedule D (Form 1040)Understanding Form 8949

Form 8949 is the transaction detail sheet. On it you list each sale of a capital asset, including the description, date acquired, date sold, proceeds, cost basis, and any adjustment codes. The IRS requires you to separate transactions into short‑term and long‑term, and further into those where the basis was reported to the IRS (covered) and those where it wasn't.

Common adjustment codes include wash sale disallowed (code W), incorrect basis reported (code B), or a nondeductible loss from personal‑use property (code L). These adjustments flow into the gain or loss column and ensure Schedule D receives the correct net figures.

You can file multiple Forms 8949 if you have many transactions, but the totals from each category are combined into one number per category on Schedule D. If you receive a consolidated 1099‑B from your broker, the statement may already separate short‑term and long‑term trades with adjustments, making it easier to transfer the information.

Reporting Investment Sales

Stocks, Bonds, ETFs, and Mutual Funds

Sales of these securities are reported on Form 8949 and summarized on Schedule D. Your broker will typically provide the cost basis for covered securities, but for noncovered securities you must track the basis yourself. If you reinvested dividends, those additional purchases increase your basis and must be factored in to avoid overpaying tax.

For mutual fund capital gain distributions, you generally report them directly on Form 1040 line 7 (capital gain distributions) if you didn't have any other capital transactions, but if you also sold shares, you'll need Schedule D.

Real Estate Sales

Selling a primary residence may qualify for the $250,000/$500,000 exclusion if you meet the ownership and use tests, but you still might need to report the sale on Form 8949 and Schedule D if you receive a Form 1099‑S or if the gain exceeds the exclusion. Rental property sales involve depreciation recapture (Unrecaptured Section 1250 gain) which is reported on Schedule D.

Cryptocurrency and Digital Assets

The IRS treats virtual currencies as property. Every taxable exchange — selling crypto for fiat, trading one coin for another, or using crypto to buy goods — triggers a capital gain or loss. You must report these on Form 8949 with the fair market value and basis. The 2026 Form 1040 includes a digital asset question that you must answer, but the actual gain or loss goes on Schedule D. We cover this in more detail below.

If you’re curious about how these gains impact your overall tax picture, you can use a paycheck calculator to model your after‑tax income. Sites like FreeAiden also offer free online tools to estimate your total tax liability.

Capital Loss Deduction Rules

If your capital losses exceed your capital gains, you have a net capital loss. The IRS allows you to deduct up to $3,000 of that loss ($1,500 if married filing separately) against other income, such as wages or interest. Any remaining loss beyond that limit is not wasted — it carries forward to future years.

For example, if you have a net short‑term loss of $4,000 and no gains, you can deduct $3,000 on your 2026 return, and the remaining $1,000 is carried to 2027 as a short‑term capital loss. This annual limit has remained unchanged for years and applies to both short‑term and long‑term net losses combined.

Keep in mind that the $3,000 deduction reduces your ordinary income, which can be valuable, but you must apply it even if you don't itemize. According to IRS guidance, you must report the carryover on next year's Schedule D.

Capital Loss Carryovers

When you have a capital loss greater than the annual deduction limit, the unused portion is carried forward indefinitely until it's fully used. The character of the loss (short‑term or long‑term) is preserved in the carryover. The ordering rules require that short‑term losses are used first to offset future short‑term gains, and long‑term losses against long‑term gains.

Let's say you have a $9,000 net long‑term loss in 2026 and no gains. You deduct $3,000, carrying $6,000 forward to 2027 as a long‑term loss. In 2027, you have a $4,000 long‑term gain and $1,000 short‑term gain. The carryover long‑term loss first offsets the $4,000 long‑term gain, leaving $2,000 of long‑term loss that then offsets the $1,000 short‑term gain, resulting in a net $1,000 long‑term loss, which you can deduct up to $3,000. The IRS Schedule D instructions include a Capital Loss Carryover Worksheet to help track these amounts each year.

See How Capital Gains Affect Your Take‑Home Pay

Use our free salary after taxes calculator to estimate your net income after capital gains taxes.

Calculate Your Take‑Home PaySchedule D and Form 1040

The net capital gain or loss from Schedule D flows directly to Form 1040, line 7. If you have a net gain, it increases your adjusted gross income (AGI), potentially affecting your eligibility for other tax benefits. A net loss (up to $3,000) reduces your AGI, which could increase your refund or lower your balance due.

In addition, you may need to complete the Qualified Dividends and Capital Gain Tax Worksheet or the Schedule D Tax Worksheet if you have long‑term gains or qualified dividends. These worksheets calculate the tax using the preferential rates, ensuring you don't pay ordinary income tax rates on long‑term gains.

Your filing status also plays a role. Married couples filing jointly combine their capital gains and losses, while those filing separately must each report their own transactions and the $1,500 loss limit applies. Community property states may have special rules for assets acquired during marriage.

Special Rules for Cryptocurrency and Digital Assets

The IRS has made it clear that virtual currency is property, not currency. Every time you sell, exchange, or spend crypto, you realize a gain or loss equal to the difference between the fair market value and your basis. That means even buying a coffee with Bitcoin is a taxable event.

All crypto transactions go on Form 8949. The 2026 tax return asks: “At any time during the tax year, did you receive, sell, exchange, or otherwise dispose of any digital asset?” Answering yes requires you to include the resulting capital gain or loss on Schedule D. There is no de minimis exception, and the IRS has increased enforcement, so accurate recordkeeping of every trade, including airdrops and hard forks, is essential.

For wash sales, the wash sale rule does not currently apply to crypto because the IRS classifies it as property, not a security. However, Congress has considered changes, so stay alert. Always refer to the official IRS website for the latest updates.

Common Schedule D Filing Mistakes

- Forgetting to adjust basis for wash sales. If your broker reported the sale but you had a wash sale, you must manually enter the disallowed loss on Form 8949 using code W.

- Omitting crypto transactions. Many taxpayers assume small crypto trades don't count, but every exchange is reportable.

- Missing capital loss carryovers. If you had a loss last year, you must bring the carryover into this year's Schedule D. Failing to do so means you overpay tax.

- Incorrectly classifying short‑term vs. long‑term. Check the trade date carefully; holding period errors change tax rates.

- Not reporting real estate sales that qualify for the exclusion. Even if the gain is fully excluded, you may still need to report the sale if you received a Form 1099‑S.

- Double‑counting reinvested dividends. Those dividends increase your cost basis; not accounting for them leads to inflated gains.

Schedule D (Form 1040): Capital Gains and Losses Explained – FAQs

1. Do I need to file Schedule D if my broker reports everything on a 1099‑B?

Yes, you still must report the transactions on Form 8949 and summarize them on Schedule D. The IRS receives a copy of your 1099‑B, and your return must match. Even if no gain or loss is shown, you need to include it.

2. Can I deduct a loss on the sale of my personal residence?

No. A loss on the sale of a personal residence is not deductible. Only losses from investment or business property can be used. Gains up to the exclusion limits may be tax‑free, however.

3. What happens if I forget to include a capital loss carryover?

You may overstate your income and pay more tax than you owe. You can file an amended return using Form 1040‑X to correct it. Keep your carryover worksheet so you don't lose track of unused losses.

4. Are capital gain distributions from mutual funds reported on Schedule D?

Not always. If you didn't sell any shares and had no other capital transactions, you can report capital gain distributions directly on Form 1040 line 7 without Schedule D. Check the Form 1040 instructions for conditions.

5. How does the wash sale rule affect my Schedule D?

If you sell a security at a loss and buy substantially identical securities within 30 days before or after, the loss is disallowed. You must add the disallowed amount to the basis of the new shares on Form 8949 with code W. This increases your gain or decreases your loss when you eventually sell.

6. Do I pay state tax on capital gains reported on Schedule D?

Most states tax capital gains as ordinary income. You'll need to check your state's tax rules. Federal Schedule D calculates only your federal taxable gain; state reporting may require a separate schedule.

7. Is cryptocurrency mining income reported on Schedule D?

Mining income is generally ordinary income at the fair market value on the day you received it, reported on Schedule 1 or Schedule C. When you later sell or exchange the mined coins, the gain or loss goes on Form 8949 and Schedule D.

8. Can I use capital losses to offset capital gain distributions?

Yes. Capital losses first offset capital gain distributions (which are treated as long‑term gains) and any other capital gains before the $3,000 ordinary income deduction applies.

9. What if I sold an inherited asset?

Inherited property generally receives a stepped‑up basis to the fair market value on the date of death. Your gain or loss is the difference between that stepped‑up basis and the sale price. Report it on Form 8949 and Schedule D.

10. How do I report a worthless stock?

If a stock becomes completely worthless, you can claim a capital loss as if you sold it for $0 on the last day of the tax year. Enter it on Form 8949 with the appropriate date and a basis. The holding period determines if it's short‑term or long‑term.

Getting Schedule D Right

Preparation is everything when it comes to reporting capital gains and losses. Start by gathering every Form 1099‑B, 1099‑S, and crypto exchange report you received. Create a simple spreadsheet or use tax software to separate transactions by holding period and adjust for wash sales and reinvested dividends.

Before you file, double‑check that you've included capital loss carryovers from last year’s return. If you sold real estate, verify whether you qualify for the home sale exclusion and whether you received a 1099‑S. For digital assets, be sure you can support your basis and the fair market value at the time of each trade.

When you transfer totals to Schedule D, compare the net gain or loss to your own records. If you have a large loss, plan how the $3,000 deduction and carryover will affect future years. Using a reliable paycheck calculator can help you see how your after‑tax income changes once you factor in capital gains. Accurate reporting now saves you from IRS notices later.

Take Control of Your Investment Taxes

Explore more free resources and tools to calculate your take‑home pay after accounting for capital gains and other income.

Explore Tax Resources