IRS Schedule B: A Complete Guide to Reporting Interest, Dividends, and Foreign Accounts

Last Updated: 2026 | Reviewed by a financial analyst and IRS tax education researcher.

Understanding exactly what to report on your tax return keeps you compliant and prevents costly mistakes. Schedule B is one of those forms that sounds more complicated than it actually is. It’s simply the place where you list interest income, dividend income, and answer a few critical foreign financial account questions. This guide walks you through each part, based on official IRS Schedule B instructions, so you can file with confidence.

Schedule B is an IRS tax form that taxpayers use to report taxable interest and ordinary dividends over $1,500, and to disclose foreign bank accounts or foreign trusts. It's filed with Form 1040 when certain income or reporting thresholds are met.

Table of Contents

- What Is Schedule B?

- Who Must File Schedule B?

- When Is Schedule B Required?

- Types of Interest Income

- Types of Dividend Income

- How Schedule B Works with Form 1040

- How to Fill Out Schedule B Step-by-Step

- Foreign Financial Account Reporting

- Schedule B vs Other IRS Schedules

- Common Schedule B Mistakes

- Electronic Filing

- Examples of Completing Schedule B

- Schedule B FAQs

- Completing Schedule B With Confidence

What Is Schedule B?

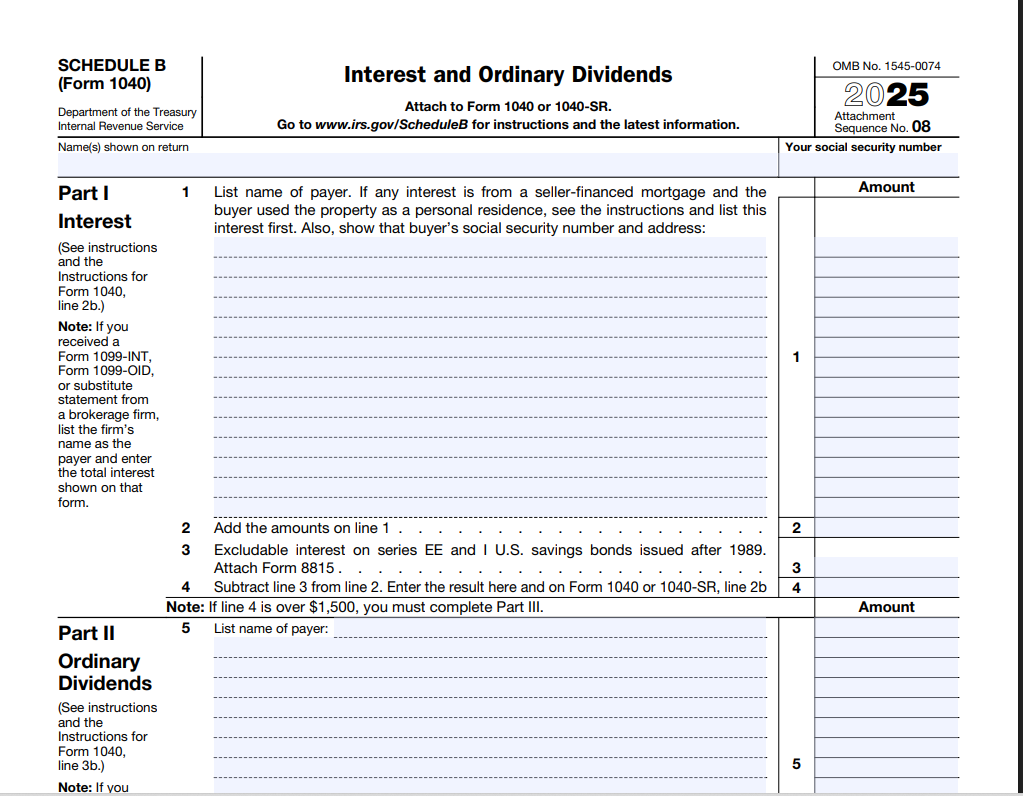

Schedule B (Form 1040) is an attachment to your individual tax return. Its official title is “Interest and Ordinary Dividends.” The form is divided into three parts. Part I covers interest income, Part II reports ordinary dividends, and Part III asks questions about foreign accounts and foreign trusts. Even if you don’t owe additional tax because of it, filing Schedule B correctly shows the IRS where your money came from.

Most people encounter Schedule B when they have more than $1,500 in combined interest and dividends for the year. However, the foreign account questions can require the form even if your income is below that threshold. This guide is based on official IRS Schedule B instructions and educational tax resources.

Who Must File Schedule B?

According to IRS guidance, you must attach Schedule B to your Form 1040 if any of these apply:

- Your total taxable interest income exceeds $1,500.

- Your total ordinary dividends exceed $1,500.

- You had a foreign bank or financial account with a balance over $10,000 at any time during the year.

- You received a distribution from, or were the grantor of, or transferor to, a foreign trust.

If none of these situations fit, you generally do not need Schedule B. But always read the instructions for exceptions. Sometimes a small amount of foreign interest or a trust relationship triggers the filing requirement.

When Is Schedule B Required?

The form becomes mandatory the moment your reportable totals cross the $1,500 mark. This limit applies separately to interest and to dividends. For example, if you earned $1,200 in bank interest and $400 in dividends, you would need Schedule B because the combined dividends and interest both individually fall below $1,500 but together exceed? No, the rule is each category independently: if taxable interest is $1,500 or less, you don't list each payer on Schedule B, but still report it on 1040 line 2; Schedule B is required if taxable interest is over $1,500 OR ordinary dividends over $1,500. So $1,200 interest and $400 dividends means neither category exceeds $1,500, so Schedule B is not required for income reporting. But if you have foreign account > $10k, you still file Schedule B to answer Part III questions.

Also, certain taxpayers must file Schedule B regardless of income amount, such as those who have signature authority over a foreign account, or received foreign trust distributions.

Types of Interest Income

Part I of Schedule B asks you to list the name of each payer and the amount of taxable interest you received. Here are the most common forms of interest that must be reported:

Taxable Interest

- Bank and credit union accounts: Checking, savings, and money market interest.

- Certificates of deposit (CDs): Interest earned, even if not withdrawn.

- Corporate bonds: Interest from bonds issued by companies.

- Seller-financed mortgages: Interest received on a private mortgage you hold.

- U.S. Treasury bills and notes: Interest is taxable for federal purposes.

- Foreign interest: Interest from non-U.S. banks is fully taxable.

Tax-Exempt Interest

Tax-exempt interest, such as from municipal bonds, is reported in a separate box on Schedule B but not included in the taxable total. The IRS still wants to see it, so don't leave it off entirely. Enter the total on line 1 of Part I; the worksheet then subtracts it to arrive at taxable interest.

According to IRS guidance, you must still list the payer and amount of tax-exempt interest even though it isn't taxed.

Types of Dividend Income

Part II covers ordinary dividends. Most dividends from stocks, mutual funds, and real estate investment trusts (REITs) fall into this category. Even if some of those dividends qualify for lower capital gains rates, you report the full ordinary amount on Schedule B.

Ordinary Dividends

Your Form 1099-DIV box 1a shows the total ordinary dividends. That's the number you list. Qualified dividends are a subset and are computed later on your Form 1040. Do not subtract qualified dividends on Schedule B.

Dividends from credit unions and certain cooperatives are not called dividends; they are reported as interest. So check your forms carefully.

How Schedule B Works with Form 1040

Schedule B flows directly into your Form 1040. The total taxable interest from Schedule B line 4 goes to Form 1040 line 2b. Total ordinary dividends from line 6 goes to Form 1040 line 3b. If you have qualified dividends, they are carried to line 3a of the 1040 after you complete the Qualified Dividends and Capital Gain Tax Worksheet.

Using a paycheck calculator to estimate your income tax can help you see how the extra interest and dividends impact your tax bracket. It’s helpful to calculate your take-home pay after accounting for this income. You can also use a salary after taxes calculator to incorporate your investment earnings into a complete picture.

How to Fill Out Schedule B Step-by-Step

Let's walk through each part of the form. Take your time and gather your 1099-INT, 1099-DIV, and any foreign account statements.

Part I: Interest Income

Line 1: List the name of each payer. If you have more entries than space, attach a separate statement with the same information.

Enter the amount of taxable interest from each. Add them together and write the total on line 2.

Line 3: Excludable interest from series EE or I U.S. savings bonds used for higher education. Follow the instructions to see if you qualify.

Line 4: Subtract line 3 from line 2. This is your total taxable interest that moves to Form 1040.

If you have any tax-exempt interest, list it at the bottom of Part I and include the total. Don't add it into the taxable line.

Example: You received $1,820 from First National Bank and $230 from a credit union. Both are taxable. List both payers, sum to $2,050. No exclusion applies, so line 4 is $2,050.

Part II: Ordinary Dividends

Line 5: List the payer names and ordinary dividend amounts from Form 1099-DIV box 1a. Add them all up and enter the total on line 6.

That total also goes to Form 1040 line 3b. Your qualified dividends will be entered directly on Form 1040 line 3a after using the worksheet.

Part III: Foreign Accounts and Foreign Trusts

This section is crucial, and the IRS scrutinizes it closely. Read each question carefully.

Question 7a: “At any time during the tax year, did you have a financial interest in or signature authority over a financial account located in a foreign country?” Check “Yes” if the aggregate value of all such accounts exceeded $10,000 at any point in the year. Even a brief spike counts.

If Yes, you may need to file FinCEN Form 114 (FBAR) electronically. Schedule B asks for the country name(s).

Question 8: Asks if you received a distribution from, or were the grantor of, or transferor to, a foreign trust. Answer honestly. If yes, you may need to file Form 3520 or 3520-A.

Foreign Financial Account Reporting

The foreign account questions on Schedule B are a gateway to additional reporting obligations. If you check “Yes” on 7a, you might need to e-file an FBAR. The FBAR is separate from your tax return and has its own due date. You’ll report the account’s maximum value during the year. This requirement exists even if the account didn’t generate any taxable interest.

If you have foreign financial assets above certain thresholds, you might also need Form 8938, Statement of Specified Foreign Financial Assets. Schedule B doesn’t replace that form; it’s just the first place you declare the existence of such accounts.

Schedule B vs Other IRS Schedules

| Schedule | Purpose |

|---|---|

| Schedule B | Interest and ordinary dividends, foreign accounts |

| Schedule D | Capital gains and losses from investments |

| Schedule C | Business profit or loss (self-employment) |

| Schedule E | Rental real estate, royalties, partnerships |

Many taxpayers file multiple schedules. For example, you might have interest on Schedule B and capital gains on Schedule D from the sale of stocks. They are independent but both affect your adjusted gross income.

Common Schedule B Mistakes

- Missing tax-exempt interest. Even if it’s not taxed, you still must list it in Part I or risk an IRS notice.

- Forgetting foreign account checkbox. If you accidentally answer “No” when you should have said “Yes,” penalties can apply. Amend with Form 1040-X if needed.

- Confusing qualified and ordinary dividends. Only the ordinary amount goes on Schedule B. Don’t report only qualified dividends or net amounts.

- Omitting small payers. If the total exceeds $1,500, you must list every payer individually, even if one paid only $1.

- Not using the correct payer name. Use the name exactly as it appears on the 1099-INT or 1099-DIV.

Electronic Filing

IRS e-file supports Schedule B seamlessly. When you use software or a professional, the interview process will flag when you need Schedule B. The software automatically fills in lines and transfers totals to Form 1040. If you’re filing on paper, be sure to attach Schedule B behind Form 1040 in the order number sequence.

Examples of Completing Schedule B

Scenario 1 – Simple interest over $1,500: Maria has a savings account that earned $1,650 and a CD that earned $200. Both are taxable. She lists both payers on Schedule B, totals $1,850 on line 4, and transfers it to her 1040. She has no foreign accounts.

Scenario 2 – Dividends plus foreign account: James received $900 in ordinary dividends (no interest). His total dividends are under $1,500, but he has a foreign bank account in Canada that hit $12,000 during the year. He must file Schedule B solely to answer “Yes” to 7a and list Canada. He also needs to e-file the FBAR.

Want to see how investment income changes your paycheck? Calculate your estimated take-home pay

If you use a free tool like the one at freeaiden.com to estimate taxes, remember to still verify with IRS forms.

Schedule B FAQs

What is Schedule B?

Schedule B is an IRS form used with Form 1040 to report taxable interest and ordinary dividends that exceed $1,500 in total. It also asks whether you have foreign bank accounts or interests in foreign trusts.

Who needs to file Schedule B?

You need to file Schedule B if your taxable interest and/or ordinary dividends total over $1,500, or if you had a foreign bank account with a balance over $10,000 at any time in the year, received a distribution from a foreign trust, or had an interest in a foreign trust.

Do I need Schedule B if my bank interest is under $1,500?

If your total taxable interest and ordinary dividends are both $1,500 or less, and you are not required to report foreign accounts or trusts, you generally do not need to file Schedule B. However, you still must report the income on your Form 1040.

What types of interest must be reported on Schedule B?

You must report taxable interest from bank accounts, credit union accounts, certificates of deposit, corporate bonds, and interest from seller-financed mortgages. Tax‑exempt interest is listed separately but not taxed.

Are ordinary dividends always taxable?

Ordinary dividends are generally taxable as ordinary income unless they are classified as qualified dividends, which are taxed at lower capital gains rates. Schedule B reports the total ordinary dividends; the qualified portion is figured on Form 1040.

What triggers the foreign account questions on Schedule B?

If you held an interest in or signature authority over a foreign financial account with a balance exceeding $10,000 at any time during the year, you must check “Yes” in Part III and may need to file FinCEN Form 114 (FBAR). Questions about foreign trusts also apply.

Can I e-file Schedule B?

Yes. Schedule B is fully supported by IRS e-file. Most commercial tax software and authorized e-file providers include the form automatically when interest, dividends, or foreign account thresholds require it.

Where do I find my interest and dividend totals?

Look at Form 1099-INT for interest income and Form 1099-DIV for dividend income. Your brokerage year-end summary also lists these amounts. If you have multiple payers, list each on Schedule B separately.

What happens if I forget to check the foreign account box?

Failing to answer the foreign account questions truthfully can lead to serious penalties. The IRS cross‑checks FBAR filings and Form 8938 with Schedule B. If you discover an omission, amend your return using Form 1040-X.

Is Schedule B the same as Schedule D?

No. Schedule B reports interest and dividend income. Schedule D reports capital gains and losses from the sale of investments. Both may be needed if you sell stocks or other assets, but they serve different purposes.

Review the official IRS Schedule B instructions before filing your tax return.

View Official Schedule B InformationCompleting Schedule B With Confidence

Getting Schedule B right means carefully checking your interest and dividend totals, listing every payer, and answering the foreign account questions truthfully. Set aside your 1099-INT and 1099-DIV forms before you start. If you had a foreign account that exceeded $10,000 even for a day, check “Yes” on line 7a. It’s better to file the FBAR unnecessarily than to miss the disclosure. Keep copies of your brokerage statements and bank records with your tax file.

Using a reliable calculator to forecast your tax can also help. Calculate your take-home pay after investment income