Schedule 1 (Form 1040): What It Is and How to Fill It Out

Filing your federal tax return often means more than just filling out Form 1040. If you earned money outside a regular job or qualify for certain deductions that lower your taxable income, you’ll likely need Schedule 1 (Form 1040). This guide walks you through every part of Schedule 1, from reporting additional income to claiming adjustments that reduce your adjusted gross income (AGI).

Table of Contents

- Schedule 1 (Form 1040): What It Is and How to Fill It Out

- Who Needs to File Schedule 1?

- When Is Schedule 1 Required?

- Understanding Additional Income

- Understanding Adjustments to Income

- How Schedule 1 Affects Adjusted Gross Income (AGI)

- How to Fill Out Schedule 1 Step-by-Step

- Line-by-Line Instructions

- How Schedule 1 Connects to Form 1040

- Common Filing Mistakes

- Electronic Filing Tips

- Download Schedule 1 (Form 1040)

- Schedule 1 (Form 1040): What It Is and How to Fill It Out – FAQs

Schedule 1 (Form 1040): What It Is and How to Fill It Out

Schedule 1 is an attachment to your individual income tax return, Form 1040. According to IRS guidance, it serves two specific purposes. Part I collects additional income that isn’t listed on the main Form 1040 lines—things like business profit, rental real estate earnings, unemployment pay, and gambling winnings. Part II lists adjustments to income, often called “above-the-line” deductions, that can reduce your total income before you calculate adjusted gross income (AGI).

Instead of cluttering Form 1040 with dozens of extra lines, the IRS designed Schedule 1 to keep the main form clean while capturing the full picture of your finances. You simply fill out the parts that apply to you, and then transfer the totals to Form 1040. This guide, based on official IRS Schedule 1 (Form 1040) instructions and educational tax resources, shows exactly how to do that without the headache.

Who Needs to File Schedule 1?

You must file Schedule 1 if you have any type of additional income that belongs in Part I or if you qualify for one or more adjustments in Part II. It’s not an optional form when those conditions exist. Even if you only have a small amount of freelance income or a few hundred dollars in gambling winnings, the IRS expects Schedule 1 to be included with your Form 1040.

Some of the most common filers who need Schedule 1 include:

- Freelancers, gig workers, and small business owners who report business income on Schedule C.

- Landlords with rental income.

- Anyone who received unemployment compensation (note: unemployment is taxable at the federal level, but some states do not tax it).

- Taxpayers who sold investments and have capital gains or other gains not reported elsewhere.

- Individuals who won prizes, awards, or gambling income.

- People paying or receiving alimony under pre-2019 divorce agreements (post-2018 agreements are no longer taxable or deductible).

- Taxpayers claiming deductions like the student loan interest deduction, IRA contributions, or health savings account contributions.

- Educators who spent money on classroom supplies.

- Self-employed individuals deducting health insurance premiums or part of self-employment tax.

If none of these apply to you and your only income is from wages on a W-2, you probably won’t need Schedule 1. But it’s always wise to review the form each year because a life change—like starting a side hustle or paying student loan interest—can trigger the filing requirement.

When Is Schedule 1 Required?

Schedule 1 becomes a required attachment the moment you have an entry on any line in Part I or Part II. There is no minimum dollar amount below which you can skip it. For example, if you earned $150 from a weekend side gig and received a 1099-NEC, that business income must be reported on Schedule 1, line 3. Similarly, if you made a $500 deductible IRA contribution and want to lower your taxable income, you claim it in Part II, line 19.

According to the IRS instructions for Form 1040, you attach Schedule 1 directly behind your main Form 1040 when you file on paper. When you file electronically, the software handles the attachment automatically. The requirement is triggered by the presence of the income or adjustment, not by a specific income threshold.

Understanding Additional Income

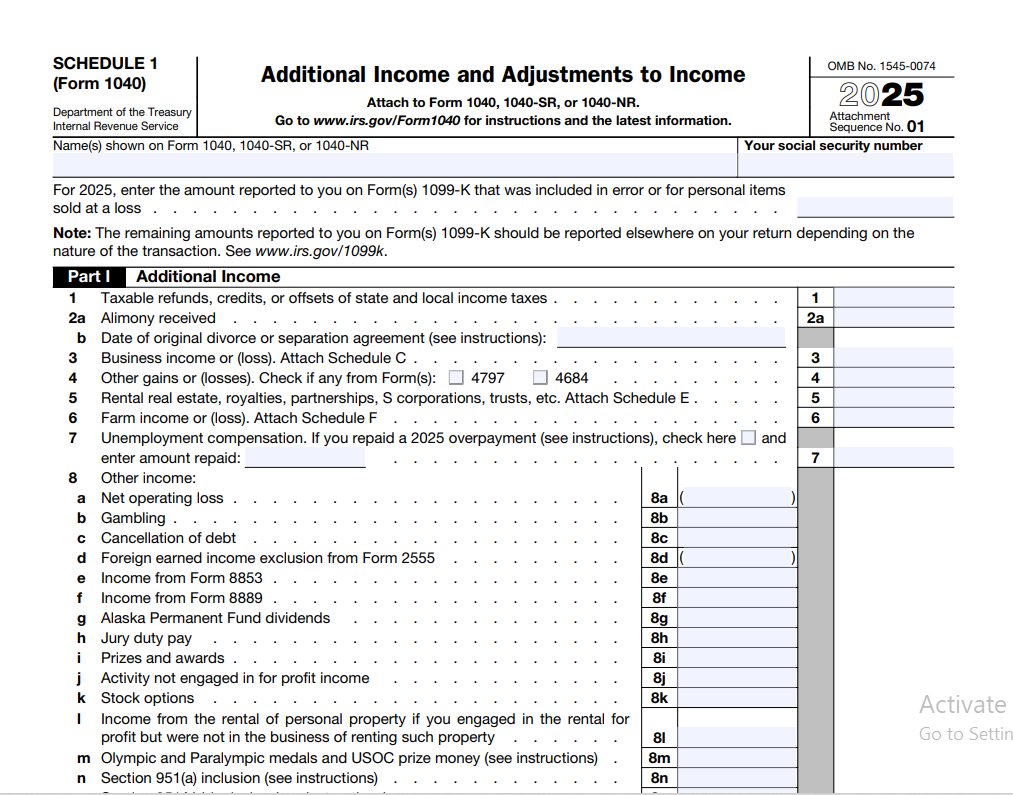

Part I of Schedule 1 captures income that doesn’t fit neatly into the wages, salaries, and tips line on Form 1040. This can include money you earned through self-employment, property rentals, unemployment benefits, and even certain legal settlements. The IRS wants a complete picture of your financial activity, and Schedule 1 provides the space to report it.

Each type of additional income has its own line on the form, and many require you to attach an additional supporting schedule. For instance, business income typically flows from Schedule C to Schedule 1, line 3. Rental real estate income arrives from Schedule E. The form itself does not replace those detailed schedules; it simply gathers the final profit or loss figures and carries them forward to your main tax return.

Here are some of the most frequent additional income types you might encounter:

| Income Type | Schedule 1 Line | Common Source Document | Notes |

|---|---|---|---|

| Business income (or loss) | Line 3 | Schedule C, 1099-NEC | Report net profit/loss from self-employment. |

| Rental real estate, royalties, partnerships, S corporations | Line 5 | Schedule E | Include rental income, royalties, or pass-through entity income. |

| Unemployment compensation | Line 7 | Form 1099-G | Taxable at federal level; some states do not tax it. |

| Gambling winnings | Line 8 | Form W-2G | Report full amount; losses may be deductible as itemized deductions. |

| Prizes and awards | Line 8 | Form 1099-MISC | Taxable unless excluded by law (e.g., certain scholarships). |

| Alimony received (pre-2019 agreements) | Line 2a | Court order or agreement | Post-2018 agreements are not taxable. |

| Taxable refunds, credits, or offsets of state and local income taxes | Line 1 | Form 1099-G | Only if you itemized deductions in the prior year. |

| Farm income (or loss) | Line 6 | Schedule F | Report net farm profit/loss. |

| Other income (jury duty pay, certain scholarships, cancellation of debt, hobby income) | Line 8 | Various | Include Form 1099-C for canceled debt. |

When you receive a 1099 form for any of these, don’t assume it’s automatically tax-free. The income still needs to be reported on Schedule 1 even if you didn’t get a form. Keeping your own records throughout the year is the safest approach.

Understanding Adjustments to Income

Part II of Schedule 1 is where you claim adjustments that directly lower your total income before you arrive at adjusted gross income. These are often called “above-the-line” deductions because they reduce AGI without requiring you to itemize. That’s a big advantage: you can take the standard deduction and still benefit from these adjustments.

According to IRS guidance, adjustments to income include popular deductions such as the student loan interest deduction, the IRA deduction, educator expenses, and the health savings account deduction. Self-employed individuals can also deduct a portion of their self-employment tax, health insurance premiums, and retirement plan contributions.

Each adjustment has eligibility rules and dollar limits. For example, the student loan interest deduction allows you to reduce your income by up to $2,500 if you paid interest on a qualified student loan and your income falls below certain thresholds ($75,000–$90,000 for single filers in 2025). The educator expense deduction lets eligible teachers and school staff deduct up to $300 of unreimbursed classroom expenses. These amounts may change slightly year to year, so always check the latest Form 1040 instructions for the current limits.

Here are common adjustments and where they appear on Schedule 1:

| Adjustment | Line | Maximum Amount (2025 tax year, filed in 2026) | Notes |

|---|---|---|---|

| Educator expenses | Line 10 | $300 ($600 if married filing jointly and both spouses are educators) | For eligible K-12 teachers, instructors, counselors, principals, or aides. |

| Health Savings Account (HSA) deduction | Line 12 | Varies by coverage type (self-only: $4,150; family: $8,300 in 2025) | Attach Form 8889. |

| Deductible part of self-employment tax | Line 14 | 50% of your self-employment tax | Only the employer portion (7.65%) is deductible. |

| Self-employed retirement plans (SEP, SIMPLE, etc.) | Line 15 | Contribution limits apply (e.g., SEP: up to 25% of net earnings, max $69,000 in 2025) | Attach Form 5305-SEP if applicable. |

| Self-employed health insurance deduction | Line 16 | Amount of premiums paid | For medical, dental, and long-term care insurance. |

| IRA deduction | Line 19 | Up to $7,000 ($8,000 if age 50 or over) | Phase-outs apply based on income and workplace retirement plan coverage. |

| Student loan interest deduction | Line 20 | Up to $2,500 | Phase-out: $75,000–$90,000 (single), $155,000–$185,000 (married filing jointly). |

| Alimony paid (pre-2019 agreements) | Line 18a | Actual amount paid | Post-2018 agreements are not deductible. |

| Archer MSA deduction | Line 21 | Varies | Attach Form 8853. |

| Other adjustments (e.g., jury duty pay turned over to employer, repayment of supplemental unemployment benefits) | Line 22 | Varies | Include explanations for "other" adjustments. |

These adjustments directly reduce your taxable income before you compute the rest of your return. That’s why it’s so important to claim every adjustment you’re entitled to—missing one could mean paying more tax than you actually owe.

How Schedule 1 Affects Adjusted Gross Income (AGI)

Your adjusted gross income is the foundation for many tax calculations, including eligibility for credits, deductions, and even your tax bracket. Schedule 1 plays a direct role in shaping that number. Additional income from Part I adds to your total income, while adjustments from Part II subtract from it.

Here’s the flow in plain terms: you start with the income you reported on Form 1040 lines 1a through 7 (wages, interest, dividends, etc.). Then you add the total from Schedule 1, line 9 (the sum of all your Part I additional income). That gives you the total income on Form 1040, line 8. Next, you subtract the total adjustments from Schedule 1, line 26. The result is your adjusted gross income on Form 1040, line 11.

This is a critical step because AGI determines whether you can take certain tax breaks. For example, the student loan interest deduction phases out at higher AGI levels. A lower AGI can mean a bigger deduction and less tax. That’s why correctly reporting every adjustment on Schedule 1 matters—it’s your chance to legally reduce your income before tax rates are applied. Once you know your AGI, you can use a paycheck calculator to estimate how much of your income you actually keep after taxes.

How to Fill Out Schedule 1 Step-by-Step

Filling out Schedule 1 is straightforward once you know which lines apply to your situation. The form itself is only one page, split into two parts. You’ll need your income statements (W-2s, 1099s) and records of any deductible expenses or contributions.

Begin by downloading the most recent version of the form from the IRS website. Then follow these steps:

- Complete Part I – Additional Income. Go through lines 1 through 8. Enter the amount for any income type that applies. If a line doesn’t apply, leave it blank. Attach any required supporting schedules (like Schedule C or E).

- Add the amounts in Part I. Write the total on line 9. This total will later go to Form 1040, line 8.

- Move to Part II – Adjustments to Income. Review lines 10 through 23. Enter the amounts for adjustments you are eligible to claim. Some lines require additional forms or calculations; follow the line instructions carefully.

- Total your adjustments. Add all the entries in Part II and put the sum on line 26.

- Transfer the totals to Form 1040. The line 9 total goes to Form 1040, line 8. The line 26 total goes to Form 1040, line 10. Double-check these transfers—this is where many errors happen.

Keep in mind that the line numbers may shift slightly from year to year. The official instructions for the tax year you’re filing always have the final say.

Line-by-Line Instructions

Let’s walk through each line of Schedule 1 so you know exactly what goes where. This breakdown follows the current 2025 tax year format (used when filing in 2026).

Part I – Additional Income

Line 1: Taxable refunds, credits, or offsets of state and local income taxes. You only enter an amount here if you itemized deductions last year and received a state tax refund. If you took the standard deduction, your refund is not taxable.

Line 2a: Alimony received. Only for divorce or separation agreements executed before 2019. Post-2018 agreements are not taxable.

Line 3: Business income or loss. Attach Schedule C. This is where freelancers and gig workers report their net profit.

Line 4: Other gains or losses. Use Form 4797 if you sold business property.

Line 5: Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E.

Line 6: Farm income or loss. Attach Schedule F.

Line 7: Unemployment compensation. You’ll receive Form 1099-G showing the amount. Taxable at the federal level; some states do not tax it.

Line 8: Other income. This is a catch-all for items like gambling winnings (Form W-2G), prizes, awards, jury duty pay, cancellation of debt (Form 1099-C), and certain scholarship amounts. List the type and amount.

Line 9: Total additional income. Add lines 1 through 8 and enter the total here.

Part II – Adjustments to Income

Line 10: Educator expenses. Up to $300 for eligible educators ($600 if married filing jointly and both spouses are educators).

Line 11: Certain business expenses of reservists, performing artists, and fee-based government officials. Follow Form 2106 for unreimbursed employee expenses.

Line 12: Health Savings Account deduction. Attach Form 8889. Limits: $4,150 (self-only), $8,300 (family) in 2025.

Line 13: Moving expenses for members of the Armed Forces. Only active-duty military moving due to orders. Civilian moving expenses are no longer deductible.

Line 14: Deductible part of self-employment tax. Calculate using Schedule SE. Only 50% of the employer portion (7.65%) is deductible.

Line 15: Self-employed SEP, SIMPLE, and qualified plans. Enter contributions made to your own retirement plan. SEP limit: up to 25% of net earnings, max $69,000 in 2025.

Line 16: Self-employed health insurance deduction. Premiums you paid for medical, dental, and long-term care insurance.

Line 17: Penalty on early withdrawal of savings. Reported on Form 1099-INT.

Line 18a: Alimony paid. For pre-2019 agreements only.

Line 19: IRA deduction. Attach Form 8606 if required. Limits: $7,000 ($8,000 if age 50+). Phase-outs apply based on income and workplace retirement plan coverage.

Line 20: Student loan interest deduction. Use Form 1098-E. Up to $2,500. Phase-out: $75,000–$90,000 (single), $155,000–$185,000 (married filing jointly).

Line 21: Archer MSA deduction. Attach Form 8853.

Line 22: Other adjustments. Include jury duty pay you turned over to your employer, repayment of supplemental unemployment benefits, or other eligible adjustments.

Line 23: Total adjustments to income. Add lines 10 through 22.

How Schedule 1 Connects to Form 1040

The numbers you write on Schedule 1 don’t stay there. They flow directly onto your Form 1040 and determine your AGI. This connection is mechanical but important to understand.

(wages, interest, dividends, etc.)

(total additional income)

(total adjustments to income)

Making a mistake on Schedule 1 can ripple through your entire return. Always verify that the transferred numbers match exactly. If you’re using tax software, it will handle the transfer for you, but you should still review the final AGI figure. Many people use a salary after taxes calculator to see how that AGI translates into take-home pay after withholding and deductions.

Common Filing Mistakes

Even careful taxpayers slip up on Schedule 1. The IRS sees these errors frequently, and they can delay refunds or trigger notices.

- Forgetting to attach the schedule. If you have additional income, Schedule 1 isn’t optional. An incomplete filing can cause processing delays.

- Reporting business income on the wrong line. Always use line 3 for business profit or loss from Schedule C, not the “other income” line.

- Missing unemployment income. Some taxpayers assume unemployment isn’t taxable and leave it off. It is taxable at the federal level and belongs on line 7.

- Skipping adjustments you qualify for. For instance, educators sometimes overlook the $300 deduction because they don’t see it promoted heavily.

- Transposing numbers. The total from line 9 goes to Form 1040 line 8, and line 26 goes to Form 1040 line 10. Swapping these can throw off your entire AGI calculation.

- Not keeping supporting documents. The IRS may ask for proof of your adjustments. Save Forms 1098-E, 5498, and receipts.

- Ignoring state-specific rules. For example, some states do not tax unemployment benefits, but the federal government does.

- Assuming all 1099 income is taxable. Some 1099 forms (e.g., 1099-INT for municipal bond interest) may report non-taxable income. Always check the instructions.

Calculate Your Take-Home Pay

Electronic Filing Tips

Electronic filing practically eliminates the risk of forgetting to attach Schedule 1 because the software generates it based on your entries. If you enter a 1099-NEC for freelance work, the program will automatically populate Schedule 1, line 3, and transfer the total to Form 1040. The same goes for student loan interest and IRA deductions.

Still, review the electronic version of your return before you hit submit. Make sure the numbers in Part I and Part II reflect your records. If you use the IRS Free File program or a commercial provider, the system will guide you through each line, but it’s your responsibility to confirm that everything is accurate. User input errors (e.g., wrong amounts, missing forms) can still occur even with software.

Review the official IRS instructions before filing.

Schedule 1 (Form 1040): What It Is and How to Fill It Out – FAQs

What is Schedule 1 (Form 1040) used for?

It’s used to report additional income (like business or rental earnings) and to claim adjustments to income that reduce your AGI. Both parts feed directly into Form 1040.

Who must file Schedule 1?

Anyone with additional income listed in Part I or who qualifies for adjustments in Part II must file it. It becomes a required attachment when any line applies.

Is unemployment compensation always reported on Schedule 1?

Yes, unemployment benefits are taxable income at the federal level and go on Schedule 1, line 7. However, some states do not tax unemployment benefits, so check your state’s rules.

Can I deduct student loan interest even if I take the standard deduction?

Absolutely. The student loan interest deduction is an adjustment to income, so you claim it on Schedule 1, line 20, regardless of whether you itemize. However, this deduction phases out at higher income levels (e.g., $75,000–$90,000 for single filers in 2025).

How does Schedule 1 affect my tax refund or amount owed?

Additional income may increase your tax liability, while adjustments lower your AGI and can reduce your tax. The net effect depends on your specific entries.

What line on Schedule 1 do I use for gambling winnings?

Gambling winnings are reported on line 8, “Other income.” List the type and the amount. You may need to attach additional statements if required.

Where can I find the official Schedule 1 instructions?

The IRS publishes the instructions with the Form 1040 instruction booklet. You can find them at IRS.gov/forms-pubs.

Do I need to file Schedule 1 if I only have a small side gig?

Yes. Any net profit from self-employment, no matter how small, must be reported on Schedule 1, line 3. It’s not a minimum-dollar exemption form.

Are alimony payments reported on Schedule 1?

Only alimony received or paid under divorce or separation agreements executed before 2019 is reported on Schedule 1 (Line 2a for received, Line 18a for paid). For agreements after 2018, alimony is no longer taxable or deductible under federal tax law.

Can I file Schedule 1 electronically?

Yes. Almost all tax preparation software supports it. The program will include Schedule 1 automatically when you enter applicable income or adjustments. However, always review your return for accuracy before submitting.

Getting Schedule 1 Right

Before you file, walk through a quick mental checklist. Confirm that every additional income source you received is accounted for in Part I. Look again at Part II and ask yourself: Did you pay student loan interest? Contribute to an IRA? Pay for your own health insurance as a self-employed person? Those adjustments can make a real difference in your final tax bill.

Keep your supporting documents organized—Forms 1099-G, 1098-E, Schedule C, and any receipts for educator expenses. If the IRS ever questions an entry, those records are your best defense. And remember, the official form and instructions are always available on IRS.gov.

For more free tax tools, you can explore resources like FreeAiden. If you want to see how your AGI translates into your actual take-home pay, try our paycheck calculator and enter your salary details. Accurate filing starts with understanding every number on your return.