Schedule SE: Self-Employment Tax Explained and How to Fill It Out

Filing taxes as a self-employed person can feel like learning a new language. You already worry about income tax, and then another form appears: Schedule SE. It stands for self-employment tax, and it often surprises new freelancers and small business owners. If you earned money outside of a traditional job where your employer withheld Social Security and Medicare taxes, the IRS still wants those contributions. That is exactly what Schedule SE calculates.

Table of Contents

- What Is Schedule SE?

- Who Must File Schedule SE?

- What Is Self-Employment Tax?

- How Schedule SE Works

- Who Doesn’t Need to File Schedule SE?

- Schedule SE Filing Thresholds

- Short Schedule SE vs Long Schedule SE

- How to Fill Out Schedule SE Step-by-Step

- Calculating Self-Employment Tax

- Social Security and Medicare Tax Details

- Deduction for One-Half of Self-Employment Tax

- Schedule SE and Form 1040

- Schedule SE for Freelancers & Gig Workers

- Schedule SE for LLC Owners

- Common Schedule SE Mistakes

- FAQs

- Practical Schedule SE Takeaways

What Is Schedule SE?

Schedule SE (Form 1040) is the IRS form where you figure your self-employment tax. This tax consists of Social Security and Medicare taxes for individuals who work for themselves. When you have a regular job, your employer withholds these taxes from your paycheck and matches them. As your own boss, you are responsible for both the employee and employer portions—collectively called self-employment tax.

The form takes your net profit from self-employment (usually from Schedule C, Schedule F, or Schedule K-1) and calculates how much you owe. It then separates the total into the Social Security portion and the Medicare portion. Most importantly, it automatically computes the deductible part you can subtract on your Form 1040. According to IRS guidance, this deduction helps level the playing field between employees and the self-employed.

Who Must File Schedule SE?

You must attach Schedule SE to your Form 1040 if your net earnings from self-employment were $400 or more during the tax year. That $400 threshold applies to your total self-employment income across all businesses or freelance activities. Even if you also have a regular job where Social Security taxes were already withheld, you still file Schedule SE if your side gig made $400 or more in net profit.

The requirement also covers church employees who earned $108.28 or more in wages subject to SECA (Self-Employment Contributions Act) tax. Independent contractors, sole proprietors, single-member LLC owners, and partners in a partnership generally need to file. The key is that you carry on a trade or business as a sole proprietor or an independent contractor. If you only received a one-time payment for a hobby that isn’t a regular business, you might not have to file, but the line can be blurry. Always check current IRS instructions.

What Is Self-Employment Tax?

Self-employment tax is how the IRS collects Social Security and Medicare contributions from people who work for themselves. For employees, the combined rate is 7.65% from the employee and 7.65% from the employer, totaling 15.3%. When you are self-employed, you pay the entire 15.3% yourself. However, the tax code softens this by letting you deduct half of it later.

The tax has two parts: 12.4% for Social Security and 2.9% for Medicare. Social Security tax only applies to net earnings up to a maximum amount that changes annually. For 2025, that wage base was $176,100. The IRS will adjust it for 2026; check the official announcement before filing. Medicare tax applies to every dollar of net earnings—there is no cap. An Additional Medicare Tax of 0.9% may apply to earnings above $200,000 (single) or $250,000 (married filing jointly), but that is calculated on Form 8959, not on Schedule SE.

How Schedule SE Works

Schedule SE takes your net profit and multiplies it by 92.35% to account for the fact that employees don’t pay Social Security and Medicare tax on their employer’s share. The resulting number is your “net earnings from self-employment.” Then the form applies the 12.4% Social Security rate to the portion up to the annual limit and the 2.9% Medicare rate to all of it. It also separates these so you can see exactly what you pay for each program.

After computing the total tax, you transfer that figure to Form 1040, Schedule 2, line 4. Then on Schedule 1, you enter one-half of your self-employment tax as an adjustment to income. That lowers your adjusted gross income and can reduce your income tax bill. The entire flow is designed to mirror the payroll tax system in a fair way for self-employed taxpayers.

From Schedule C or other business income.

To get net earnings.

Up to Social Security cap.

On Schedule 1, line 15.

Who Doesn’t Need to File Schedule SE?

You are exempt from filing Schedule SE if your net earnings from self-employment are less than $400. If your only self-employment income was from a church and it was below $108.28, you may not have to file. Also, certain limited partners in a partnership may not owe self-employment tax on their distributive share if they are not active in the business, but this requires careful reading of IRS rules. Additionally, if your only self-employment income is from foreign sources and you qualify for the foreign earned income exclusion and you are not liable for self-employment tax under a totalization agreement, you might be exempt. Always confirm with a tax professional.

Retired individuals with no current self-employment activity, or those whose only income is from investments, generally do not need Schedule SE. The form is specifically about earned income from a trade or business you actively run.

Schedule SE Filing Thresholds

The $400 threshold is a net earnings figure, not gross revenue. If you made $3,000 in freelance income but had $2,800 in deductible business expenses, your net profit is $200. Because $200 is under $400, you do not need to file Schedule SE (though you still may need to report the income). The threshold triggers the filing requirement for self-employment tax specifically.

For church employees, the threshold is $108.28. This applies to wages subject to SECA tax, not self-employment earnings from a business. If you received a W-2 with box 14 showing SECA wages, you would use Schedule SE to compute the tax on that income.

Short Schedule SE vs Long Schedule SE

The IRS provides two sections on Schedule SE: Section A (Short Schedule SE) and Section B (Long Schedule SE). You can use the short version if your net earnings from self-employment are under the Social Security wage base limit, you did not use an optional method to figure net earnings, and you did not receive wages subject to social security tax that reduce the amount subject to self-employment tax. Most self-employed individuals with moderate incomes qualify for Section A. It saves time because you skip the detailed Social Security wage base calculation.

Section B is for those whose net earnings plus any wages exceed the Social Security maximum, or who use optional methods (like the farm optional method). It requires you to input your total wages subject to Social Security tax and then compute how much of your self-employment income is still subject to the 12.4% Social Security portion. Even with high earnings, the Medicare portion of 2.9% applies to all net earnings.

How to Fill Out Schedule SE Step-by-Step

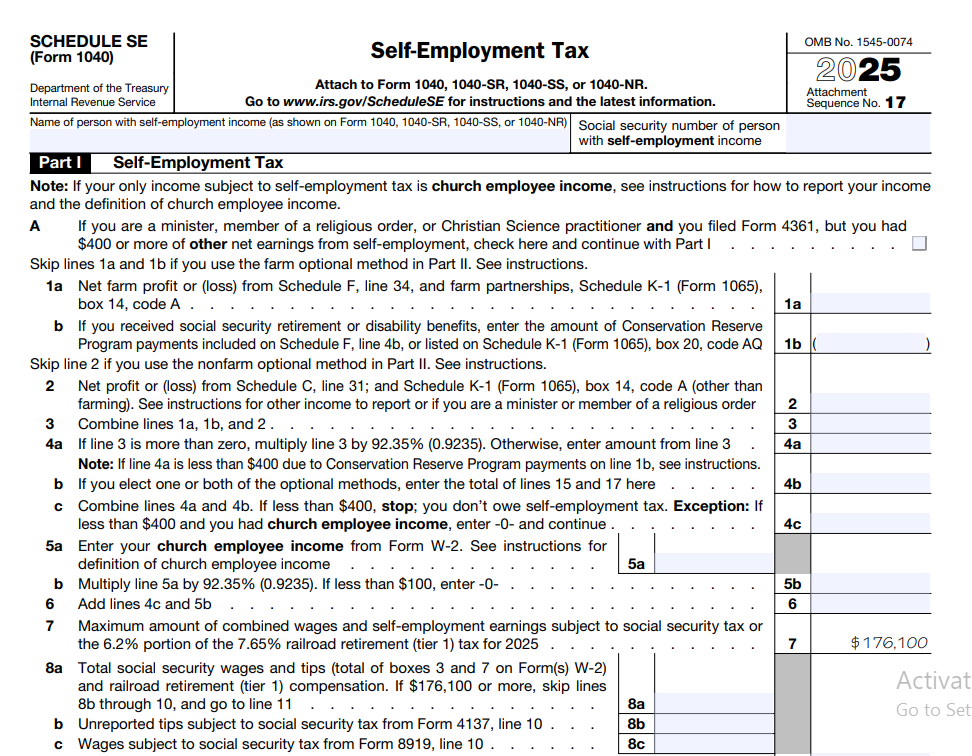

Let’s walk through filling out the form using a realistic example. Imagine you run a small consulting business as a sole proprietor, and your Schedule C net profit is $52,000. You have no other earned income and no church wages. Here is how each line works, following the official IRS Schedule SE instructions.

Part I – Line 1a and 1b

If you have net farm profit from Schedule F, you enter that on line 1a. For most non-farm sole proprietors and freelancers, line 1b is where you put your net profit or (loss) from Schedule C, line 31. In our example, $52,000 goes on line 1b. If you have multiple businesses, combine the net profits and enter the total.

Line 2 – Combine Lines 1a and 1b

Add the figures from lines 1a and 1b. For our example, $52,000. If you have a loss, you would still enter it, but a negative number may reduce other self-employment earnings; however, a net loss can result in zero self-employment tax if the total is under $400. The form handles that.

Line 3 – Net Profit Multiplied by 92.35%

Multiply line 2 by 92.35% (0.9235). This step adjusts for the employer-equivalent portion. $52,000 × 0.9235 = $48,022. If the result is less than $400, you stop here; you do not owe self-employment tax. In our case, it’s well above $400.

Line 4 – Combine with Optional Methods if Any

Most people skip the optional methods and simply enter the amount from line 3 on line 4. The optional methods let you increase net earnings to earn Social Security credits, but they are rarely needed if you have substantial income.

Line 5 – Self-Employment Tax

For Short Schedule SE, you multiply line 4 by 15.3% (0.153). $48,022 × 0.153 = $7,347.37. That is your self-employment tax. In Section B, you would break it down into Social Security and Medicare parts. Here, the short form does the math in one step.

Line 6 – Deduction for One-Half of Self-Employment Tax

Multiply line 5 by 50% (0.50). $7,347.37 × 0.5 = $3,673.68. This amount goes on Schedule 1, line 15, as an adjustment to income.

You then transfer the line 5 total to Schedule 2, line 4, and it becomes part of your total tax on Form 1040. The form’s layout makes it straightforward once you have your net profit figure.

| Schedule SE Line | Description | Example Amount |

|---|---|---|

| Line 1b | Net profit from Schedule C | $52,000 |

| Line 2 | Combined net earnings | $52,000 |

| Line 3 | 92.35% of line 2 | $48,022 |

| Line 5 | Self-employment tax (15.3%) | $7,347.37 |

| Line 6 | One-half deductible | $3,673.68 |

Calculating Self-Employment Tax

To calculate self-employment tax manually, you need your total net earnings from self-employment. Take your net profit (after business expenses), multiply by 92.35%. If the result is under $400, you owe no self-employment tax. Above that, apply 15.3%. However, for Social Security, only the first $X of combined wages and self-employment income is taxed, with X being the annual wage base limit. If you have wages from a job, your self-employment Social Security tax may be reduced because your employer already withheld up to the limit. Schedule SE Section B handles that coordination.

For example, if you have a day job that paid $150,000 in wages and you also earned $30,000 in self-employment profit, the Social Security tax would only apply to the portion of your self-employment earnings that, when added to your wages, doesn’t exceed the wage base. Medicare tax would still apply to all $30,000 of self-employment profit (after 92.35% adjustment).

Social Security Tax and Medicare Tax Explained

Social Security tax: This is 12.4% of your net earnings up to the annual limit. It funds retirement, disability, and survivor benefits. As a self-employed person, you pay the full 12.4%, but you can deduct half. The wage base for 2026 will be announced by the IRS; for 2025 it was $176,100. If you earn more than the limit in combined wages and self-employment income, no further Social Security tax is due on the excess. If you have no wages, the limit applies only to your self-employment earnings.

Medicare tax: The rate is 2.9% on all net earnings—no cap. This funds hospital insurance. Self-employed individuals also pay the full 2.9% but deduct half. Once your combined earned income exceeds $200,000 (single) or $250,000 (married filing jointly), you owe an additional 0.9% on the excess, calculated on Form 8959. That extra amount is not part of Schedule SE.

Deduction for One-Half of Self-Employment Tax

One of the most valuable aspects of Schedule SE is the line that gives you back half of your self-employment tax. This is an above-the-line deduction, meaning you can take it even if you don’t itemize. It reduces your adjusted gross income (AGI), which can lower your taxable income and potentially help you qualify for other tax benefits. The deduction is calculated automatically on Schedule SE, line 6, and you simply enter that number on Schedule 1 (Form 1040), line 15. It is not a credit, but it directly offsets your income for income tax purposes.

For the earlier example with $7,347.37 in self-employment tax, you would deduct $3,673.68 from your total income. This mimics the way an employer’s share of payroll taxes is not included in an employee’s taxable wages. It’s a straightforward yet powerful adjustment.

Curious how self-employment tax affects your take-home pay? Use our paycheck calculator to compare scenarios as an employee versus self-employed, or calculate your take-home pay after self-employment tax and deductions.

Estimate Your Self-Employment IncomeSchedule SE and Form 1040

Schedule SE works hand in hand with Form 1040. After you finish Schedule SE, you report the self-employment tax on Schedule 2 (Additional Taxes), line 4. That amount gets added to your total tax liability. Then, on Schedule 1 (Additional Income and Adjustments to Income), line 15, you enter the deductible portion of self-employment tax. This flows to Form 1040, line 10, as an adjustment to income, lowering your AGI.

If you make estimated tax payments or have withholding, those payments are applied against your total tax, including self-employment tax. That is why the IRS encourages self-employed individuals to make quarterly estimated payments using Form 1040-ES. Without these, you may face an underpayment penalty. The connection between Schedule SE and the 1040 is essential to get right, because omitting the deduction or misplacing the tax amount can lead to an incorrect return.

Schedule SE for Freelancers, Independent Contractors, Sole Proprietors, and Gig Workers

If you drive for a rideshare app, sell handmade goods online, consult, design websites, or do any freelance work, you are likely considered self-employed. The IRS treats all these activities as a trade or business if you do them regularly and for profit. Schedule SE applies to your net earnings after you deduct business expenses on Schedule C. Even if you receive a 1099-NEC or 1099-K, you must report the income and file Schedule SE if your net profit exceeds $400.

Gig workers sometimes overlook self-employment tax because their platforms do not withhold taxes like an employer would. This can lead to a large tax bill at filing time. Using a salary after taxes calculator that includes self-employment tax can help you set aside money each month. Recordkeeping is critical; keep a log of mileage, supplies, and other costs to lower your net profit and thus your self-employment tax.

Schedule SE for LLC Owners

Single-member LLCs are disregarded entities for tax purposes unless you elect otherwise. That means the IRS treats the owner as a sole proprietor, and you report business income and expenses on Schedule C. The net profit flows to Schedule SE the same as any other sole proprietor. Multi-member LLCs taxed as partnerships give each member a Schedule K-1 showing their share of ordinary business income. Generally, guaranteed payments and the partner’s distributive share of income are subject to self-employment tax. However, limited partners who do not materially participate may be exempt from self-employment tax on that income. The rules are nuanced; many LLC members end up filing Schedule SE. If you have an LLC, review the instructions for partners carefully or consult a tax professional.

Common Schedule SE Mistakes

Even experienced filers slip up on Schedule SE. Here are some errors to avoid:

- Forgetting the 92.35% multiplier: You cannot apply 15.3% directly to net profit. Missing this step overstates your tax.

- Not filing when net earnings are over $400: Some side hustlers assume a 1099-K means nothing if they don’t receive a 1099-NEC. The filing requirement is based on net profit, not the form type.

- Using the wrong section: Using Short Schedule SE when your wages plus self-employment income exceed the Social Security wage base will cause an incorrect calculation. Switch to Section B.

- Missing the deduction on Schedule 1: Failing to enter the one-half deduction leaves money on the table and increases your income tax.

- Incorrectly combining multiple businesses: You must combine all self-employment income on one Schedule SE, not file separate forms for each gig.

- Omitting church employee income: If you had SECA wages, they go on Schedule SE even if you have no other self-employment income.

Download Schedule SE (Form 1040)

Review the official IRS instructions before filing your return.

Schedule SE: Self-Employment Tax Explained and How to Fill It Out – FAQs

The self-employment tax rate remains 15.3%: 12.4% for Social Security and 2.9% for Medicare. The Social Security portion applies only to net earnings up to the annual wage base limit, which is adjusted each year. Verify the 2026 limit directly on IRS.gov. An extra 0.9% Medicare tax may apply on high earnings, but that is separate.

You can use the Short Schedule SE (Section A) if your net self-employment earnings plus any wages subject to Social Security tax are below the annual wage base limit, and you are not using an optional method to figure net earnings. Most independent contractors with moderate incomes and no wages qualify. If your combined income exceeds the limit, you must use Section B.

Yes, if your net earnings from self-employment are $400 or more, even if you already paid Social Security tax through your employer. Schedule SE Section B will account for the wages already taxed and calculate the remaining Social Security tax owed on your self-employment income, if any. Medicare tax always applies to all net self-employment earnings.

Yes, the IRS supports electronic filing of Schedule SE through tax software and authorized e-file providers. Most online tax preparation platforms include Schedule SE and automatically populate it from your Schedule C. E-filing reduces errors and speeds up your refund.

The IRS may send you a notice for underreporting self-employment tax. You could face penalties and interest. If you realize you missed it, file an amended return using Form 1040-X and attach the completed Schedule SE. Pay any additional tax as soon as possible to minimize interest charges.

If your net earnings are less than $400, you stop before calculating tax. You would not have a self-employment tax, so the deduction would be zero. If you have net earnings above $400 but a loss from another business, you combine them. A net overall loss can eliminate self-employment tax, making the deduction moot.

Yes, they are separate taxes. Income tax is calculated on your taxable income after deductions and credits. Self-employment tax is calculated on your net business earnings and is reported separately. You owe both on the same return, which can make your total tax bill higher than you might expect.

The IRS website offers a self-employment tax calculator and instructions. For broader planning, free resources like freeaiden.com provide tax estimation tools, and you can use a salary after taxes calculator to model your net pay after self-employment obligations.

Completing Schedule SE With Confidence

You do not need to dread Schedule SE. Start by gathering your net profit totals from all self-employment activities. Use a separate spreadsheet or accounting tool to track income and deductible expenses throughout the year. When tax time arrives, pull up the official IRS PDF, follow the line-by-line instructions, and double-check the 92.35% adjustment and the deduction amount. Keep a copy of the completed Schedule SE with your tax records.

Remember to factor self-employment tax into your quarterly estimated payments. A good habit is to set aside at least 25-30% of your net profit in a separate savings account to cover both income tax and self-employment tax. If you are unsure about the Social Security wage base coordination or optional methods, take the extra time to read the IRS instructions or use reputable tax software. Getting Schedule SE right ensures you build Social Security credits and avoid costly notices later.

Ready to see how much you’ll actually take home? Calculate your take-home pay with our free tool that incorporates self-employment taxes and deductions.

Try the Paycheck Calculator