Schedule E (Form 1040): Supplemental Income and Loss Explained

If you earn money outside of a regular W-2 job, the IRS expects you to report every dollar. Schedule E (Form 1040): Supplemental Income and Loss Explained is the tax form that covers income from rental real estate, royalties, partnerships, S corporations, estates, trusts, and REMICs. Many taxpayers find Schedule E confusing because it handles several different income types on a single two-page form. Getting it wrong can trigger an IRS notice, delay your refund, or leave deductions unclaimed. This guide walks you through every part of Schedule E using official IRS instructions so you can file with clarity and confidence. This guide is based on official IRS Schedule E instructions and educational tax resources.

Quick Answer

What is Schedule E (Form 1040)? Schedule E is the IRS form used to report supplemental income and loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interests in REMICs. Taxpayers attach it to Form 1040 when they receive income from these sources during the tax year. It separates passive income from earned income for proper tax treatment.

What Is Schedule E?

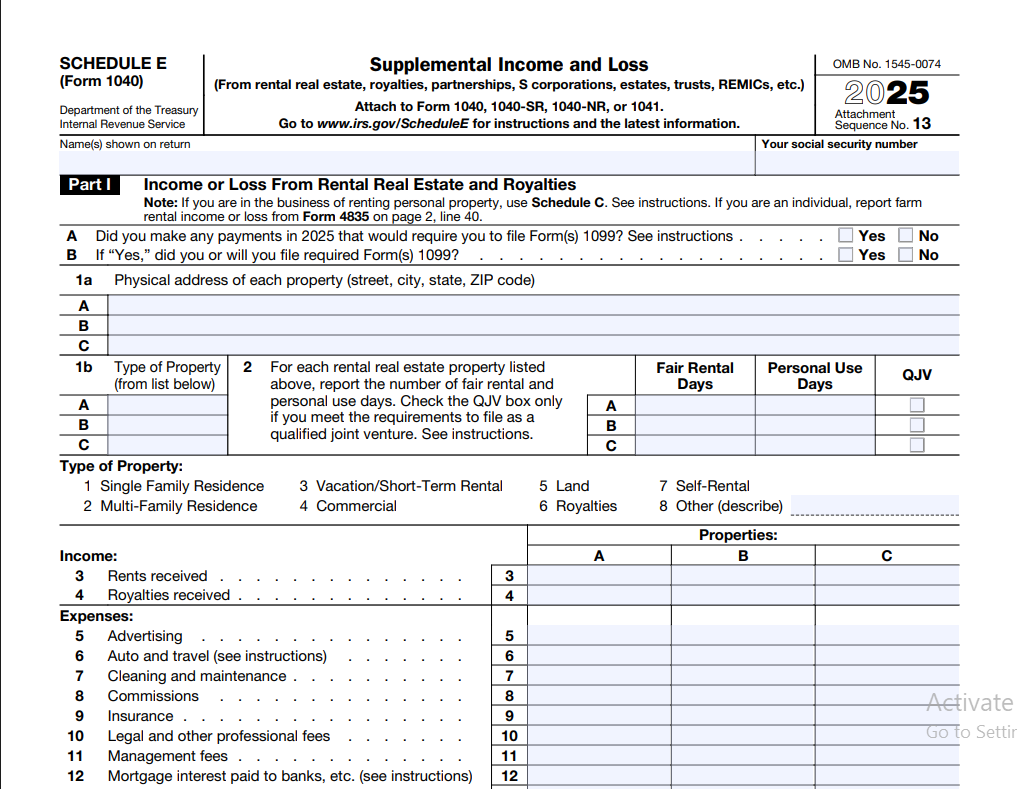

Schedule E is a supplemental form you attach to your Form 1040 individual tax return. Its official title is "Supplemental Income and Loss." The form has two pages. Page one covers rental real estate, royalties, partnerships, S corporations, estates, and trusts. Page two handles income or loss from partnerships and S corporations when additional detail is needed, plus REMIC residual interests.

The IRS designed Schedule E to separate passive and portfolio-type income from ordinary earned income like wages. Why does that matter? Because passive income faces different rules. You cannot always deduct passive losses against your regular paycheck. Understanding this distinction helps you avoid costly filing errors.

According to IRS guidance, you use Schedule E to report income from activities where you are not an active participant in day-to-day operations. Rental properties are the most common example. Even if you manage the property yourself, rental activity is generally considered passive by default unless you qualify as a real estate professional.

This form also captures income passed through to you from business entities. If you own shares in an S corporation or hold a partnership interest, the entity sends you a Schedule K-1 each year. You take the numbers from that K-1 and transfer them to your Schedule E. The income flows through to your personal return.

Who Must File Schedule E?

You must file Schedule E if any of the following apply to your tax situation during the year:

- You received rental income from real estate or personal property leased with real estate.

- You earned royalty income from mineral rights, copyrights, patents, or literary works.

- You received a Schedule K-1 from a partnership showing your share of income, deductions, or credits.

- You received a Schedule K-1 from an S corporation.

- You are a beneficiary of an estate or trust that generated income passed through to you.

- You hold a residual interest in a Real Estate Mortgage Investment Conduit, or REMIC.

Even if your rental property operated at a loss, you still must file Schedule E. The IRS wants to see the full picture of your rental activity. Failing to report a rental loss could mean you miss out on a deduction you are legally entitled to claim, subject to passive activity loss limitations.

If you had multiple rental properties, you list each property separately on Schedule E. The form provides columns for up to three properties on page one. If you own more than three, you attach additional sheets with the same format.

When Is Schedule E Required?

Schedule E must be attached to your Form 1040 whenever you have reportable supplemental income or loss from the sources listed above. There is no minimum dollar threshold. Even if you received $50 in royalty income or rented a vacation home for one week, you are required to file Schedule E.

A common point of confusion involves short-term rentals. If you rent your property for fewer than 15 days during the year and use it personally for more than 14 days, the IRS generally does not require you to report that rental income. But once you cross the 15-day rental threshold, Schedule E becomes mandatory. The rules for vacation rentals blend personal and rental use, and the IRS instructions provide worksheets to calculate the correct split.

If you receive a Schedule K-1 that shows zero income but still reports deductions or credits, you may still want to file Schedule E. Those deductions can offset other passive income. According to IRS guidance, you should file whenever a K-1 is issued to you.

Types of Income Reported on Schedule E

Schedule E covers six distinct categories of supplemental income. Each type follows its own reporting rules and has unique tax implications. Understanding the differences helps you place each income stream in the correct part of the form.

Rental Real Estate Income

Rental income includes payments you receive from tenants for the use of real property such as houses, apartments, condominiums, commercial buildings, and farmland. It also covers payments for the use of personal property like furniture or equipment when leased together with real estate.

You report gross rental income on line 3 of Schedule E. From that amount, you subtract allowable expenses such as mortgage interest, property taxes, insurance, repairs, maintenance, utilities, and depreciation. The net result, whether profit or loss, flows to your Form 1040.

Advance rent counts as income in the year you receive it, regardless of which period it covers. Security deposits are not income if you plan to return them to the tenant. However, if you keep part of a security deposit because the tenant damaged the property, that portion becomes taxable rental income in the year you retain it.

If you use a paycheck calculator to estimate your W-2 tax withholding, remember that rental income can push you into a higher bracket. Factoring supplemental income into your planning helps avoid a surprise tax bill.

Royalty Income

Royalty income comes from allowing others to use your property. Common sources include mineral rights from oil, gas, or coal extracted from your land, copyright royalties from books or music you created, and patent royalties from inventions you licensed to a manufacturer.

You report royalties on line 4 of Schedule E. Related expenses such as depletion for mineral properties, legal fees to defend a patent, or agent commissions reduce your taxable royalty amount. According to IRS guidance, you must report gross royalties before subtracting any depletion allowance. The depletion deduction then appears separately on the expense lines.

If you actively run a business around your creative work, you might need Schedule C for self-employed business income instead of Schedule E. The distinction hinges on whether you are engaged in a trade or business with regular, continuous activity versus passively receiving royalty checks.

Partnership Income

When you are a partner in a business structured as a partnership, you receive a Schedule K-1 (Form 1065) each year. The K-1 shows your distributive share of the partnership's income, deductions, credits, and other items. You transfer those amounts to Schedule E, Part II.

The partnership itself does not pay income tax. Instead, income passes through to the partners. Your K-1 might show ordinary business income, rental income, interest income, capital gains, or section 179 deductions. Each item retains its character when reported on your personal return. A capital gain on the K-1 remains a capital gain on your Schedule E and flows to your Schedule D Capital Gains and Losses when applicable.

Partnership income reporting requires careful attention. The IRS matches K-1 information against what you report. Discrepancies frequently trigger automated notices. Always enter exactly what the K-1 shows.

S Corporation Income

S corporation shareholders receive a Schedule K-1 (Form 1120-S) reporting their share of corporate income, losses, and deductions. You enter these amounts on Schedule E, Part II, using the same columns as partnership income. The reporting mechanics are similar, but S corporations have unique rules around shareholder basis, distributions, and reasonable compensation.

Unlike partnership income, S corporation income is not subject to self-employment tax. This is a key advantage. However, shareholder-employees must receive reasonable W-2 wages before taking distributions. The IRS scrutinizes S corporations that attempt to classify all compensation as distributions to avoid payroll taxes.

If your S corporation K-1 shows a loss, you can only deduct it to the extent of your stock and debt basis in the corporation. Schedule E includes basis limitation rules you must follow. Claiming a loss beyond your basis results in a suspended loss carried forward to future years.

Estate and Trust Income

Beneficiaries of estates and trusts receive a Schedule K-1 (Form 1041) showing income distributed or required to be distributed to them. This income retains its character. Interest income, dividends, and capital gains all flow through and must be reported on the appropriate forms.

You report estate and trust income on Schedule E, Part III. Unlike partnership or S corporation income, estate and trust income is reported on a separate part of the form with fewer line items. The estate or trust pays tax on income it retains. You pay tax on income distributed to you.

Estates often generate income during the administration period after someone passes away. If you are named as a beneficiary, you may receive K-1s for several years until the estate closes. Each year's K-1 must be reported on that year's Schedule E.

REMIC Income

REMIC stands for Real Estate Mortgage Investment Conduit. These are entities that hold pools of mortgages and issue securities to investors. If you own a residual interest in a REMIC, you report your share of income or loss on Schedule E, Part IV.

REMIC reporting is less common than rental or partnership income. Most taxpayers will never encounter this section. However, if you invest in mortgage-backed securities with complex structures, you may receive a Schedule Q that feeds into your Schedule E reporting. The IRS instructions provide detailed guidance for REMIC residual interest holders.

How to Fill Out Schedule E Step-by-Step

Completing Schedule E correctly starts with gathering all your documents before you sit down to file. You need your rental income and expense records, all Schedule K-1s received, and royalty statements. Working through the form systematically reduces errors.

Gather documents including rent ledgers, expense receipts, mortgage interest statements (Form 1098), property tax bills, insurance invoices, and all K-1s.

Complete Part I for each rental property. Enter the property address, number of rental days and personal use days, gross rents received, and all deductible expenses.

Calculate net rental income or loss by subtracting total expenses from gross rents. This figure moves to line 26 on the front page.

Enter royalty income on line 4 with related expenses. Include depletion if applicable for mineral rights.

Transfer K-1 amounts to Part II for partnerships and S corporations, and Part III for estates and trusts. Use the exact figures from each K-1.

Total all income and losses on lines 26 through 32. Carry the combined total to line 41 and then to your Form 1040, Schedule 1, line 5.

The key to accurate Schedule E filing is matching every entry to supporting documentation. If a K-1 shows $5,432 in ordinary business income, enter exactly $5,432. Rounding or estimating creates mismatches the IRS computer systems flag for review.

Rental Property Expenses

Rental property owners can deduct a wide range of ordinary and necessary expenses. These deductions directly reduce your taxable rental income. The more thorough your recordkeeping, the more legitimate deductions you can claim.

| Deductible Expense | Description | Schedule E Line |

|---|---|---|

| Mortgage Interest | Interest paid on loans secured by the rental property. Reported on Form 1098. | Line 12 |

| Property Taxes | Real estate taxes assessed by local government. Deductible in the year paid. | Line 11 |

| Insurance | Premiums for fire, flood, liability, and landlord insurance policies. | Line 9 |

| Repairs | Fixing leaks, painting, replacing broken windows. Must be repairs, not improvements. | Line 14 |

| Management Fees | Payments to property managers or HOA fees on rental units. | Line 8 |

| Utilities | Water, electricity, gas, internet if paid by the landlord. | Line 15 |

| Depreciation | Annual deduction for the cost of the building, not the land. | Line 18 |

| Professional Fees | Legal and accounting fees directly related to the rental activity. | Line 17 |

One of the most important distinctions in rental expense reporting is repairs versus improvements. Repairs keep the property in good operating condition. Painting a unit between tenants is a repair. Replacing the entire roof is an improvement. Repairs are fully deductible in the current year. Improvements must be capitalized and depreciated over multiple years, typically 27.5 years for residential rental property. Misclassifying an improvement as a repair is a common IRS audit trigger.

Repairs vs. Improvements: A repair fixes something broken. An improvement adds value, extends the property's useful life, or adapts it to a new use. When in doubt, ask whether the work merely restored the property to its original condition or made it better than before.

Depreciation Explained

Depreciation is an annual deduction that recovers the cost of your rental building over time. The IRS knows buildings wear out. Instead of deducting the entire purchase price in one year, you spread the deduction across the property's useful life. For residential rental real estate, that period is 27.5 years. For commercial property, it is 39 years.

You cannot depreciate land. Only the building and certain improvements qualify. When you buy a rental property, you must allocate the purchase price between land and building. A property tax assessment often provides a reasonable split. If you paid $300,000 for a rental house and the assessor values the land at $60,000, your depreciable basis is $240,000. Divided by 27.5 years, your annual depreciation deduction is approximately $8,727.

Depreciation is not optional. The IRS requires you to recapture depreciation when you sell the property, whether or not you claimed the deduction each year. Failing to take depreciation means you lose a valuable tax benefit and still face recapture tax later. If you have missed depreciation in prior years, you can file Form 3115 to catch up.

Beginning in 2026, the depreciation rules remain consistent with prior years for residential and commercial real estate. Bonus depreciation for certain qualified improvement property may apply in specific circumstances. Always verify current IRS depreciation tables when calculating your annual deduction.

Passive Activity Rules

The passive activity loss rules, found in IRC Section 469, limit your ability to deduct losses from passive activities against non-passive income like wages. Rental real estate is generally considered passive, regardless of how much time you spend managing it, unless you qualify as a real estate professional.

If your rental properties generate a net loss, you can deduct up to $25,000 of that loss against your other income if you actively participate in the rental activity. Active participation means you make management decisions such as approving tenants and setting rent. Using a property manager does not disqualify you. However, this $25,000 allowance phases out as your modified adjusted gross income exceeds $100,000 and disappears entirely at $150,000.

Losses you cannot deduct in the current year are not lost forever. They become suspended passive activity losses carried forward indefinitely. You can use them to offset future passive income or deduct them in full when you sell the property in a fully taxable transaction.

Real estate professionals who meet strict IRS criteria can treat rental activities as non-passive. To qualify, you must spend more than 750 hours per year in real property trades or businesses and more than half of your working time in those activities. Meeting this threshold allows unlimited rental losses against other income.

Partnership and S corporation income reported on Schedule E also falls under passive activity rules if you do not materially participate in the business. Your K-1 indicates whether the income or loss is passive or non-passive. Report passive amounts in the appropriate column on Schedule E to ensure proper loss limitation treatment.

Schedule E vs Schedule C

Taxpayers often confuse Schedule E and Schedule C because both can involve income earned outside of W-2 employment. The key difference lies in the nature of the activity. Schedule C reports profit or loss from a business you actively operate as a sole proprietor. Schedule E reports supplemental income from more passive or investment-oriented sources.

| Factor | Schedule E | Schedule C |

|---|---|---|

| Income Type | Rental, royalty, pass-through entity income | Active business income as sole proprietor |

| Self-Employment Tax | Generally no (except certain royalties) | Yes, on net profit over $400 |

| Passive Loss Rules | Usually applies | Generally does not apply |

| Depreciation | 27.5 or 39 year MACRS | Varies by asset class |

| Common Examples | Landlord, investor, K-1 recipient | Freelancer, gig worker, small business owner |

If you provide substantial services alongside a rental, such as daily housekeeping for a bed and breakfast, the IRS may consider that a business activity reportable on Schedule C rather than Schedule E. The threshold is whether you are primarily renting space or running a service business. For most landlords who simply collect rent and handle maintenance, Schedule C for self-employed business income is not the right form. Schedule E is correct.

Schedule E vs Schedule D

Schedule E and Schedule D Capital Gains and Losses serve different purposes but can intersect. Schedule D reports capital gains and losses from the sale of assets like stocks, bonds, and real estate held for investment. Schedule E reports ongoing income from assets you own, such as rental income or royalties, not the gain from selling them.

When you sell a rental property, the sale itself goes on Form 4797 and Schedule D, not Schedule E. However, the depreciation you claimed on Schedule E over the years is recaptured as ordinary income on Form 4797. This is why accurate Schedule E filing matters for the entire life of your investment. Every year's depreciation deduction affects your eventual tax bill upon sale.

If a partnership K-1 reports capital gains, you may need to transfer those gains to Schedule D rather than keeping them on Schedule E. The K-1 provides specific instructions. Portfolio income like Schedule B interest and dividend income also stays off Schedule E entirely. Knowing which schedule to use prevents reporting errors that delay processing.

Common Schedule E Mistakes

Even experienced taxpayers make errors on Schedule E. Here are the most frequent mistakes and how to avoid them:

- Forgetting to report all properties. Each rental property needs its own column or separate statement. Combining multiple properties into one column obscures the true performance of each investment.

- Misclassifying repairs as improvements or vice versa. Repairs are current-year deductions. Improvements must be depreciated. Getting this wrong can trigger an audit and result in back taxes plus penalties.

- Omitting depreciation. Depreciation is mandatory. The IRS assumes you claimed it even if you did not. File Form 3115 to correct missed depreciation from prior years.

- Entering K-1 amounts incorrectly. Transpose a number from a K-1 and the IRS matching system flags your return. Always double-check every digit against the K-1.

- Claiming passive losses against W-2 income without meeting the active participation or real estate professional rules. The $25,000 special allowance phases out between $100,000 and $150,000 of MAGI. Exceeding those limits means suspended losses.

- Not separating land value from building value for depreciation. Depreciating land is not allowed. Use a reasonable allocation method and document it.

- Reporting short-term rental income on Schedule C instead of Schedule E. Unless you provide substantial services, rentals go on Schedule E regardless of the rental period length.

Required Records to Keep

The IRS recommends keeping tax records for at least three years from the date you file your return. For rental property, retain records longer. Keep depreciation schedules, purchase documents, and improvement receipts for as long as you own the property plus three years after you file the return reporting its sale.

Essential Schedule E records include rent payment logs, bank statements showing deposit dates, expense receipts organized by category, mortgage interest statements (Form 1098), property tax bills, insurance invoices, management fee statements, legal and professional fee invoices, and all Schedule K-1s received from partnerships, S corporations, estates, or trusts.

Digital recordkeeping works well. Scan receipts and store them in cloud-based folders organized by tax year and property. If you use accounting software like QuickBooks, run year-end reports that match your Schedule E line items. Good records protect you in an audit and ensure you claim every deduction you deserve. If you need to calculate your take-home pay after accounting for rental profits, accurate records provide the numbers you need.

Electronic Filing

Most tax preparation software supports Schedule E e-filing. The IRS encourages electronic filing because it reduces errors, processes faster, and provides confirmation of receipt. When you e-file, the software performs validation checks that catch common Schedule E mistakes before submission.

If you file on paper, mail your complete return including Schedule E to the appropriate IRS processing center. Paper returns take longer to process, and manual data entry increases the chance of transcription errors. For 2026, the IRS continues to expand e-filing capabilities. Nearly all Schedule E situations, including multiple rental properties and K-1 reporting, can be e-filed with current tax software.

Need to estimate how rental income affects your paycheck?

Use a salary after taxes calculator to see how supplemental income changes your take-home pay. Planning ahead helps you adjust withholding and avoid an unexpected tax bill when you file.

Calculate Your Estimated Take-Home PayDownload Schedule E (Form 1040)

Get the official IRS form directly from the source. Review the official IRS instructions before filing to confirm you are using the most current version.

Download Schedule E (Form 1040) ↓This links to the official IRS PDF. Always verify you have the latest version for the tax year you are filing.

Schedule E (Form 1040): Supplemental Income and Loss Explained – FAQs

Do I need to file Schedule E if my rental property had a loss?

Yes. You must file Schedule E even when your rental property operates at a loss. The IRS requires you to report all rental activity. Filing also preserves your right to claim the loss, subject to passive activity limitations. If you do not file, you lose the opportunity to carry forward suspended losses to future tax years.

Can I deduct rental losses against my W-2 wages?

You may deduct up to $25,000 of rental real estate losses against non-passive income like W-2 wages if you actively participate in the rental activity. This allowance phases out when your modified adjusted gross income reaches $100,000 and disappears completely at $150,000. Real estate professionals who meet the 750-hour test can deduct unlimited rental losses.

What is the difference between Schedule E and Schedule C for rental income?

Schedule E reports passive rental income where you are primarily renting space. Schedule C reports business income where you provide substantial services like daily housekeeping, meals, or concierge services. Most residential landlords file Schedule E. Bed and breakfast operators and short-term rental hosts offering hotel-like amenities may need Schedule C instead.

How do I report income from a Schedule K-1 on Schedule E?

Transfer the amounts from your K-1 directly to the corresponding lines on Schedule E. Partnership and S corporation K-1s go in Part II. Estate and trust K-1s go in Part III. Enter the exact figures shown. Do not round or estimate. Each K-1 box is labeled with a code that corresponds to a specific Schedule E line. Follow the K-1 instructions carefully.

Are security deposits considered rental income?

Security deposits you intend to return to the tenant are not taxable income when received. However, if you keep any portion of the deposit because the tenant caused damage or failed to pay rent, that retained amount becomes taxable rental income in the year you apply it. Normal wear and tear does not justify keeping a deposit.

What expenses can I deduct on Schedule E for rental property?

Deductible rental expenses include mortgage interest, property taxes, insurance premiums, repairs and maintenance, property management fees, utilities you pay, advertising costs, legal and professional fees, travel to visit the property, and depreciation. All expenses must be ordinary and necessary. Keep receipts and document the business purpose of each expense.

Do I have to depreciate my rental property?

Yes. Depreciation is mandatory for rental property. The IRS treats depreciation as allowed or allowable, meaning you must recapture it when you sell even if you never claimed it. Residential rental buildings are depreciated over 27.5 years. If you missed depreciation in prior years, file IRS Form 3115 to claim a catch-up adjustment.

What are suspended passive activity losses?

Suspended passive activity losses are rental or other passive losses you could not deduct in the current year due to the passive loss limitations. These losses carry forward to future tax years. You can apply them against future passive income or deduct them in full when you sell the property that generated them in a fully taxable transaction.

Can I e-file my tax return with Schedule E?

Yes. Most commercial tax preparation software supports electronic filing of Schedule E with multiple rental properties, K-1 entries, and royalty income. The IRS e-file system accepts Schedule E as part of a complete electronically filed return. E-filing generally results in faster processing and fewer data entry errors compared to paper filing.

Where can I find free tools to help with tax planning?

Several online resources offer free tax planning tools. Websites like freeaiden.com provide access to tax calculators and educational content. For official IRS forms and instructions, always visit IRS.gov directly. Free tools can help you estimate tax liability but should not replace professional advice for complex situations.

Disclaimer: This article is for educational purposes only. Tax laws may change, and the information presented may not reflect the most current IRS guidance. Always verify information directly with the IRS at IRS.gov or consult a qualified tax professional. This content does not constitute legal or tax advice. Every tax situation is unique, and the rules discussed may apply differently based on your individual circumstances.

Before You File Schedule E

Filing Schedule E does not need to feel overwhelming. Start by collecting every document you will need. Rental ledgers, expense receipts, depreciation schedules, and all K-1s belong in your file before you open the form. Work through each section in order. Check every K-1 number twice against what you enter. Confirm that repairs and improvements are classified correctly. Claim depreciation even if it creates a larger loss this year.

If your rental losses exceed the passive activity limits, track your suspended losses. They carry forward and can save you substantial tax in future years. Keep your records organized by tax year and property. Digital folders with clear labels make this easy.

Take time to review the official IRS instructions linked in the download section above. The IRS updates forms and rules periodically, and reviewing current guidance before filing is a smart practice. For additional tax form guidance, explore our resources on Schedule A itemized deductions and other related schedules that may affect your overall tax return.