What Is IRS Schedule A?

If you pay significant medical bills, donate to charity, or own a home, you may have heard about IRS Schedule A. This form is where you list itemized deductions instead of claiming the standard deduction on your federal tax return. But what exactly is Schedule A, and when does it make sense to file it? In this guide you’ll learn exactly what IRS Schedule A is, who should use it, and how to complete each section correctly. We use official IRS instructions as our foundation, so you can move forward with clarity and confidence.

Table of Contents

- What Is IRS Schedule A?

- What Are Itemized Deductions?

- Standard Deduction vs Itemized Deduction

- Who Should File Schedule A?

- When Should You Use Schedule A?

- How Schedule A Works With Form 1040

- How to Complete Schedule A Step-by-Step

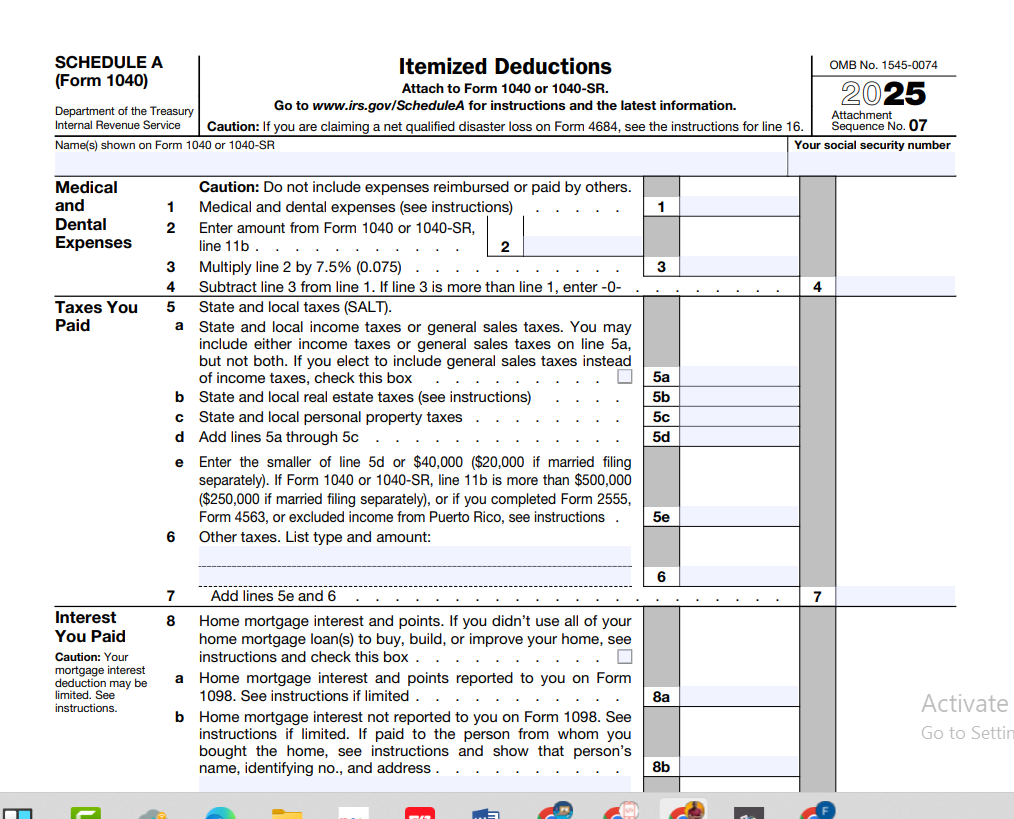

- Medical and Dental Expenses

- State and Local Tax (SALT) Deduction

- Mortgage Interest Deduction

- Gifts to Charity

- Casualty and Theft Losses

- Other Itemized Deductions

- Common Filing Mistakes

- Is Schedule A Worth Filing?

- What Is IRS Schedule A? – FAQs

- Practical Schedule A Takeaways

What Is IRS Schedule A?

IRS Schedule A is a supplementary form you attach to your Form 1040 when you choose to itemize your deductions. Instead of accepting the government’s flat standard deduction, you list specific expenses the tax code allows—such as medical costs, state and local taxes, mortgage interest, and charitable gifts. The total from Schedule A flows directly to Form 1040, reducing your adjusted gross income (AGI) and potentially lowering the income subject to tax.

According to IRS guidance, you can claim only the deductions that you actually paid during the tax year and for which you have proper records. Filing Schedule A requires a bit more paperwork, but for many taxpayers the extra effort yields a smaller tax bill.

What Are Itemized Deductions?

Itemized deductions are specific, IRS-approved expenses that reduce your taxable income. They fall into several categories that appear directly on Schedule A. Instead of taking one large standard amount, you tally real-world costs like doctor visits, property taxes, and donations. The tax code allows you to subtract the sum of these expenses from your income before figuring the tax you owe.

The most common itemized deductions include:

- Medical and dental expenses exceeding 7.5% of AGI

- State and local income or sales taxes, plus property taxes (subject to a cap)

- Home mortgage interest and points

- Gifts to qualified charities

- Casualty and theft losses from a federally declared disaster

When your total eligible expenses surpass the standard deduction for your filing status, itemizing can put money back in your pocket.

Standard Deduction vs Itemized Deduction

Every taxpayer qualifies for the standard deduction—a set dollar amount that reduces taxable income without any need to track expenses. For the 2025 tax year (the latest finalized figures at the time of writing), the standard deduction is:

| Filing Status | 2025 Standard Deduction |

|---|---|

| Single | $14,600 |

| Married Filing Jointly | $29,200 |

| Married Filing Separately | $14,600 |

| Head of Household | $21,900 |

These amounts adjust for inflation annually; the 2026 figures will be announced by the IRS later in the year. If the total of your allowable itemized deductions is greater than your standard deduction, you generally benefit from filing Schedule A. If not, the standard deduction gives you a larger reduction with less effort.

Who Should File Schedule A?

You should file Schedule A if your eligible itemized deductions exceed the standard deduction for your filing status—and if you are not required to use the standard deduction for any special reason. Typical candidates include:

- Homeowners with a mortgage and substantial property taxes

- People with high medical bills relative to their income

- Taxpayers who make significant charitable contributions

- Residents of states with high income taxes or property taxes

- Individuals who experienced a federally declared disaster loss

Even if you think you might be close, it’s worth running the numbers. This guide is based on official IRS Schedule A instructions and educational tax resources, so you can trust the framework.

When Should You Use Schedule A?

Use Schedule A when the sum of your qualifying deductions gives you a larger tax benefit than the standard deduction. This decision often depends on life events. For example, if you bought a home mid-year, paid significant mortgage interest, and gave generously to charity, itemizing could be the better choice. On the other hand, a taxpayer with no mortgage and minimal medical costs may find the standard deduction simpler and larger.

It’s also wise to check whether certain deduction limits affect you. The state and local tax (SALT) deduction is capped at $10,000 ($5,000 for married filing separately), which may limit the benefit of itemizing for high-income earners in high-tax states. However, note that the $10,000 cap is scheduled to expire after 2025. For 2026, unless Congress extends it, the cap may be lifted, which could make itemizing even more attractive. Always verify the latest tax law before filing.

How Schedule A Works With Form 1040

Schedule A is not a standalone form. You complete it and attach it to your Form 1040. The total itemized deductions you calculate on Schedule A flows to line 12 of Form 1040. This single number reduces your adjusted gross income, arriving at your taxable income. The IRS then uses that taxable income figure to determine your tax liability.

The relationship is straightforward: if you itemize, you must file Schedule A. You cannot claim itemized deductions directly on Form 1040 without it. The form also serves as a record of which deductions you are claiming, so keeping supporting documents is essential.

How to Complete Schedule A Step-by-Step

The IRS Schedule A form (Form 1040) is divided into clearly labeled sections. Here is a line-by-line overview, grounded in the official Schedule A instructions.

Schedule A Sections at a Glance

- Lines 1–4: Medical and Dental Expenses

- Lines 5–7: Taxes You Paid (SALT)

- Lines 8–10: Interest You Paid (mortgage interest, points, investment interest)

- Lines 11–14: Gifts to Charity

- Line 15: Casualty and Theft Losses

- Line 16: Other Itemized Deductions

- Line 17: Total Itemized Deductions

Begin by entering your adjusted gross income (AGI) from Form 1040, because several limits depend on it. Then work through each section. We’ll explore every major category next.

Medical and Dental Expenses

You can deduct unreimbursed medical and dental expenses for yourself, your spouse, and your dependents—but only to the extent that they exceed 7.5% of your AGI. This threshold applies to all taxpayers. For example, if your AGI is $80,000, only medical expenses above $6,000 (7.5% × $80,000) are deductible.

Qualifying expenses include payments for doctors, surgeries, prescription medications, dental treatments, vision care, mental health counseling, and certain long-term care services. You can also include miles driven for medical care and health insurance premiums (if not already paid pre-tax). Keep receipts, invoices, and mileage logs. The deductible amount is the total of all eligible expenses minus the 7.5% floor.

State and Local Tax (SALT) Deduction

The SALT deduction allows you to deduct either state and local income taxes or state and local sales taxes (but not both), plus real estate taxes and personal property taxes. However, the total deduction for all these taxes combined is limited. Through 2025, the cap is $10,000 ($5,000 for married filing separately). For 2026, this cap is set to expire under current law. If the cap lifts, you could deduct the full amount of eligible taxes paid. Verify the rule for the tax year you are filing.

When choosing between income tax and sales tax, pick the larger amount. If you live in a state with no income tax, deducting sales tax may be valuable. The IRS provides an optional sales tax calculator, or you can use actual receipts for large purchases.

Mortgage Interest Deduction

Home mortgage interest on loans secured by your main or second home is generally deductible, subject to loan limits. For mortgages taken out after December 15, 2017, you can deduct interest on up to $750,000 of acquisition debt ($375,000 if married filing separately). Older loans retain the $1 million limit. Home equity loan interest is only deductible if the loan was used to buy, build, or substantially improve the home.

You will receive Form 1098 from your lender showing the interest you paid. That amount goes on Schedule A, line 8. Points paid at closing may also be deductible over the life of the loan, and mortgage insurance premiums may be deductible if the law permits (check current status).

Gifts to Charity

Cash and non-cash donations to qualified charitable organizations are deductible. For cash gifts, you generally need a bank record or written acknowledgment. The deduction limit for cash contributions to public charities is normally 60% of your AGI, though lower limits apply for gifts to certain organizations. Non-cash items like clothing or household goods must be in good used condition or better, and you’ll need a receipt.

Special rules apply for donations of appreciated stock or vehicles. Remember that volunteer expenses (unreimbursed) such as mileage can also be deducted if you keep proper records. Always verify that the charity is IRS-recognized by using the Tax Exempt Organization Search tool on IRS.gov.

Casualty and Theft Losses

For tax years 2018 through 2025, personal casualty and theft losses are only deductible if they are attributable to a federally declared disaster. Each loss is subject to a $100 deductible per event, and the total net loss must exceed 10% of your AGI. These rules are strict, so most taxpayers will not have a deductible loss unless they experienced a major disaster. For 2026, the law may revert to allowing non-disaster losses; check the latest IRS guidance.

Other Itemized Deductions

Line 16 of Schedule A captures a handful of additional deductions, such as gambling losses (up to the amount of gambling winnings), certain unreimbursed employee expenses for qualified performing artists or fee-basis officials, and impairment-related work expenses for people with disabilities. Many miscellaneous deductions that were suspended under previous tax law are set to return after 2025. If you qualify for any of these, you’ll list the total on this line. Be sure to consult the instructions for the specific year.

Common Filing Mistakes

- Forgetting to compare to the standard deduction. Always run both numbers.

- Including non-deductible expenses. Cosmetic surgery, over-the-counter medicines (without a prescription), and personal legal fees usually do not qualify.

- Exceeding SALT cap. Only $10,000 (or $5,000 MFS) can be deducted through 2025, even if you paid more.

- Missing documentation. Charitable contributions need proof; without it the deduction can be denied.

- Miscalculating the medical floor. Deduct only the amount above 7.5% of AGI.

- Claiming the wrong home mortgage interest. Verify the loan date and amount limits.

Is Schedule A Worth Filing?

Filing Schedule A is worth the effort when your itemized deductions clearly beat the standard deduction. Even a small difference can translate into real tax savings. However, the benefit shrinks if your deductions are only slightly above the standard amount, because of the extra time and recordkeeping required. Use a paycheck calculator or your tax software to compare scenarios. Remember, the rules may change for 2026 regarding the SALT cap and miscellaneous deductions, so staying current is key.

Not sure how deductions affect your take‑home pay?

Use a free paycheck calculator to see your after-tax income with and without itemized deductions.

Calculate your estimated take-home payYou can also find free online tools at freeaiden.com to plan your finances.

Download IRS Schedule A

Review the official form before you file. Always cross-check with the latest IRS instructions.

What Is IRS Schedule A? – FAQs

No. You either take the standard deduction or you itemize on Schedule A—you cannot do both in the same year. If your itemized total is less than the standard deduction, simply claim the standard amount.

Not automatically. Only medical expenses above 7.5% of AGI are deductible. Even then, all your itemized deductions combined must exceed the standard deduction to make filing Schedule A worthwhile.

As of now, the $10,000 cap is scheduled to expire after 2025. For the 2026 tax year, there may be no cap—or Congress could extend or modify it. Always check the IRS website for the current rule.

For mortgages taken out after Dec. 15, 2017, interest on up to $750,000 of home acquisition debt is deductible. Older mortgages have a $1 million limit. Home equity interest must be used for home improvements to qualify.

Yes. For any cash donation, you need a bank record or written acknowledgment from the charity. For non-cash gifts, a receipt and description are required. Good records protect your deduction.

Through 2025, only losses from federally declared disasters are deductible. The loss must exceed $100 per event and 10% of your AGI. Personal theft losses are treated similarly.

Schedule A line 17 flows to Form 1040, line 12. This reduces your adjusted gross income, arriving at your taxable income.

Yes, health insurance premiums you pay out-of-pocket, including long-term care premiums, count as medical expenses subject to the 7.5% floor—unless they were already paid with pre-tax dollars.

There is no overall income limit, but certain deductions have phaseouts or AGI-based floors (medical expenses 7.5%, casualty losses 10%, and charitable contribution percentage limits).

If your situation is complex—multiple rental properties, large charitable donations of stock, or disaster losses—a qualified tax preparer can help you maximize deductions while staying compliant.

Practical Schedule A Takeaways

Getting your itemized deductions right starts with good records. Keep medical receipts, mortgage statements, property tax bills, and charity acknowledgments organized throughout the year. If you are close to the standard deduction threshold, small timing adjustments—like bunching charitable gifts into a single year—can push you over the edge and generate real savings.

Before you file Schedule A, open the official Schedule A (PDF) and fill it out using your actual numbers. Then compare the total to your standard deduction. A quick way to see how these deductions affect your paycheck is to calculate your take-home pay using a reliable salary calculator. Understanding your after-tax income helps you plan withholding and spending more accurately.

Remember, filing Schedule A is not about complexity—it’s about claiming what the tax code already allows you to keep. With the steps above and the official IRS guidance at your side, you can make the best decision for your financial situation.